Last Updated on Jan 11, 2024 by Harshit Singh

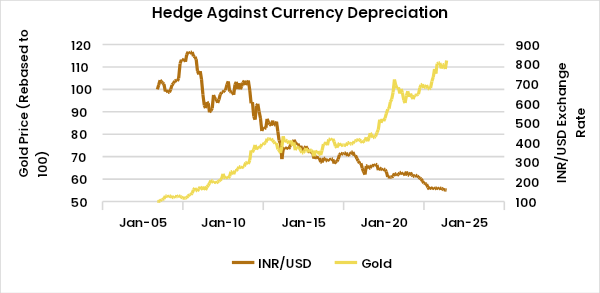

Gold acts as a hedge against currency devaluation. Gold is also considered a quasi-currency and can be easily converted into cash due to worldwide standardisation and well-developed physical markets.

INR has a natural tendency to depreciate against USD for reasons of a growth economy. India is a developing economy with supply constraints. Due to this, growth and inflation is higher than developed economies of the world. Inflation is high due to supply constraints/ technical knowhow/ labour rigidities. Due to inflation rate differentials between INDIA and US, the Indian currency depreciates against the dollar.

The Indian current account is usually in deficit, due to which the demand for dollars is higher than the supply. This demand is met by Foreign direct investment (FII) and through Foreign Portfolio Investment (FPI). As these flows are not permanent flows, RBI intervenes in the market only to control volatility in the domestic market – selling dollars to appreciate the currency from said current levels and buying dollars to depreciate the currency from said current levels. Else, the currency has the natural tendency to depreciate in these situations.

In 2000 to 2010, emerging markets grew more than developed markets, in 2010 to 2020 Developed markets outperformed the emerging markets. This decade may be emerging markets grow faster. In that case, emerging market currencies might depreciate less than the quantum by which they have depreciated in phases when developed markets have done well. Thus, Rupee could depreciate even if India and emerging markets do well, but the quantum of depreciation could be lower.

Source: Bloomberg, based on latest data available.

Table of Contents

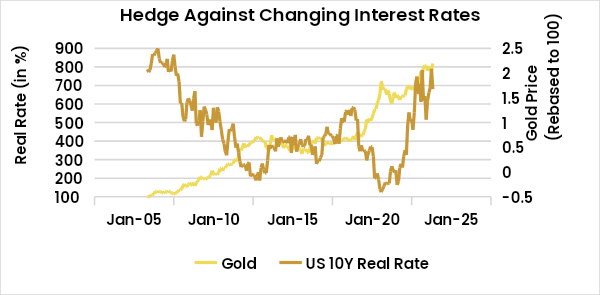

Gold – Hedge against High inflation

Gold acts as a hedge against high inflation and interest rates.

US inflation has come down to 3.1% from a 40 year high number of 8 to 9% seen in 2022. This coming down has been without having a hard landing. The period from 2008 to 2020 saw low inflation and low interest rate levels, post which it has been a high inflation and high interest rates scenario. Inflation in the UK and Eurozone has not come down as much. The UK has been facing supply side issues post BREXIT while the Russia Ukraine war has impacted supply of natural gas to the eurozone and UK.

(Source: The Economic Times)

Source: Bloomberg, based on latest available data

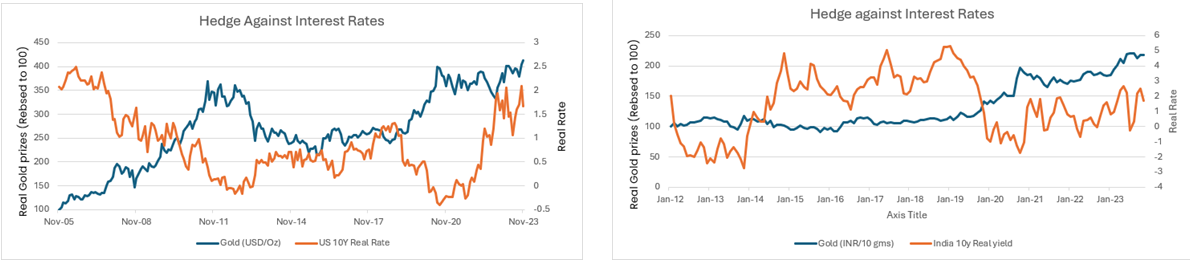

Gold prices are inversely related to real yields globally as well as in India. Currently, US inflation is back at the pre-Global Financial Crisis inflation levels of around 3% (Source: Fred Economic Data). The US is targeting 2% inflation rate. Post recent US Fed policy, the market probability for rate cuts in 2024 has increased with expectations of at least three rate cuts. Gold prices may benefit with ease in real yields and decline in interest rates in the US. Gold and interest rates are inversely proportional to each other. Though in 2000, 2004 – 2008 and in recent rate hikes, gold prices have held the risk premium, on account of economic slowdown and geo-political situations.

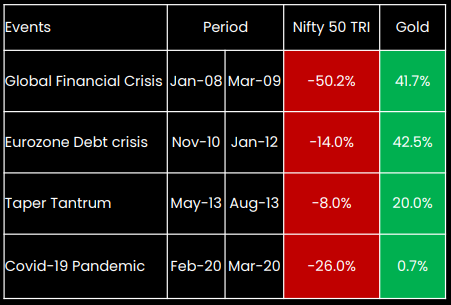

Gold – Safe haven during economic and political uncertainty

Gold’s biggest attribute is that it acts as a safe haven during times of economic and political uncertainty. Whenever there is an uncertain market environment, investors try to safeguard themselves by diversifying investment into gold. We have recent example of COVID-19 pandemic, Russia-Ukraine war and Israel-Gaza conflict. Gold rallied sharply in such instances where the global economy was affected and forced countries to take unprecedented measures.

Source: Bloomberg, NSE Indices

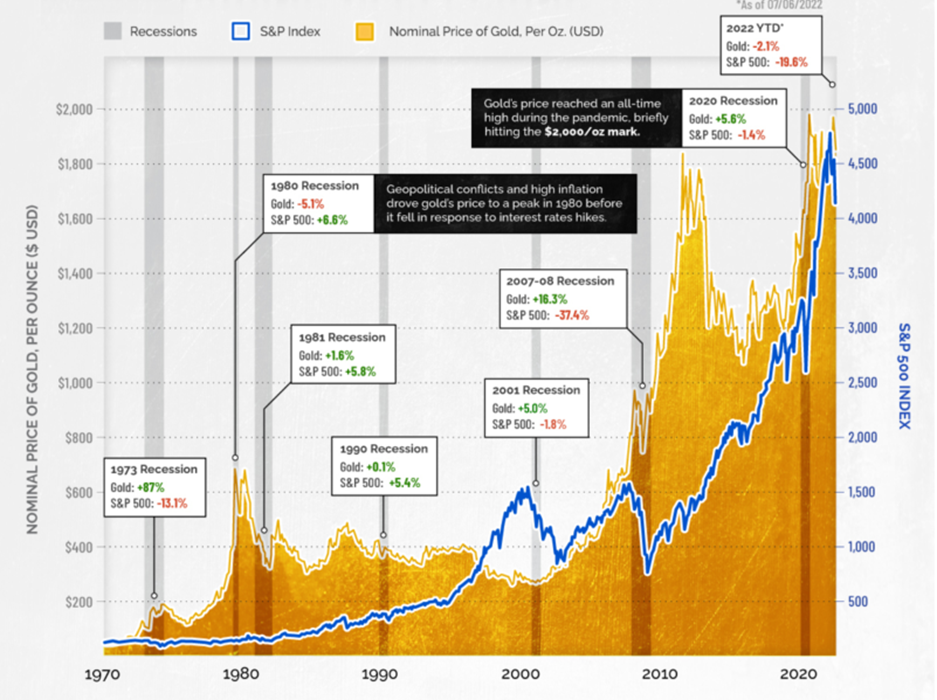

Gold performance during Recessions

Source: Bloomberg, S&P BSE Indices, based on latest data available

Low correlation of Gold to other asset classes

Gold is also considered an alternative asset to equites and helps to have a diversified and balanced portfolio. While there have been times when gold and equities have moved together, historical data shows that they have little or no correlation which makes it ideal for diversification. (Source: World Gold Council)

Going ahead we are constructive on gold prices as real yields are expected to reset from aberration high levels. Also, gold is a hedge against high inflation and currency depreciation.

Last 40 year data shows gold has yielded 1.5% CAGR more than inflation and ~1% higher than gross FD rate.

Source: Foundation of Independent Financial Advisors, based on latest data available.

Is de-dollarization happening?

It is a complex weave of dollar presence across the global trade system but any other currency to become reserve can happen over a longer period. Gold reserves of Central Banks have increased by 14%. Central Banks hold Gold to diversify investments and hedge currency depreciation.

(Source: World Gold Council)

The US dollar is a global reserve currency not by any treaty or any rule or any law. It is the strength of its economy, its open capital markets and its reputation of an institution. 50% of world trades get settled in dollars, 60% of global central bank assets are dollar assets (Source: Exim Bank India), US has invested in many countries’ bonds, many countries have borrowed from US, lent to US. There could emerge another reserve currency but the debate is open – Local currency, Brics common currency, Bitcoin, Gold- the future and the turn of events is unknown.

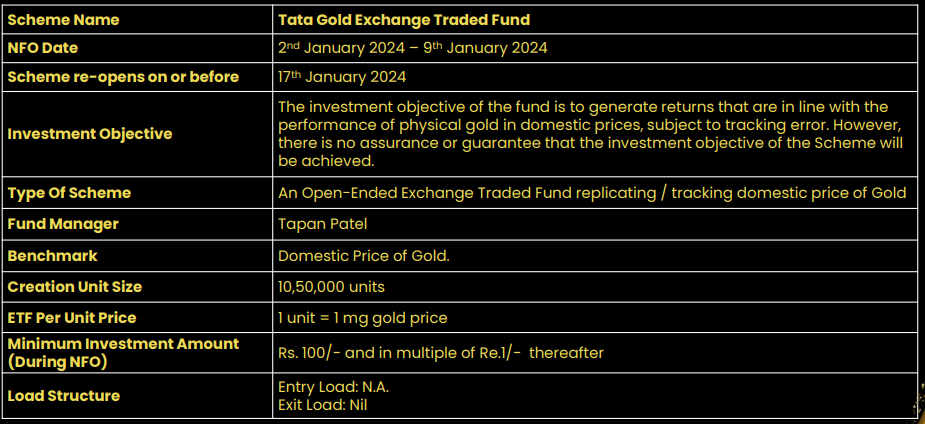

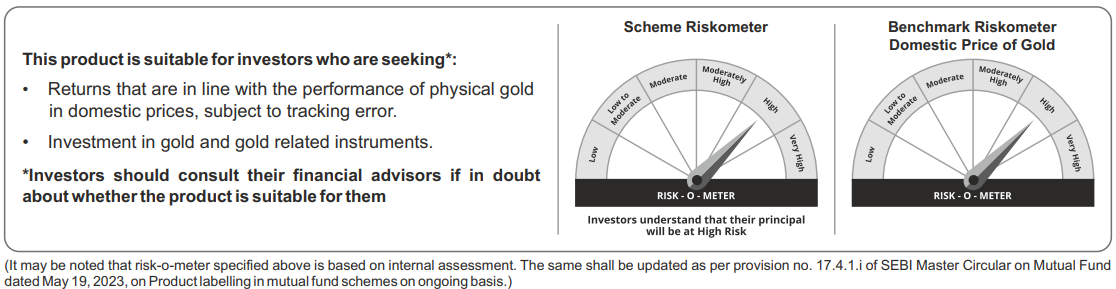

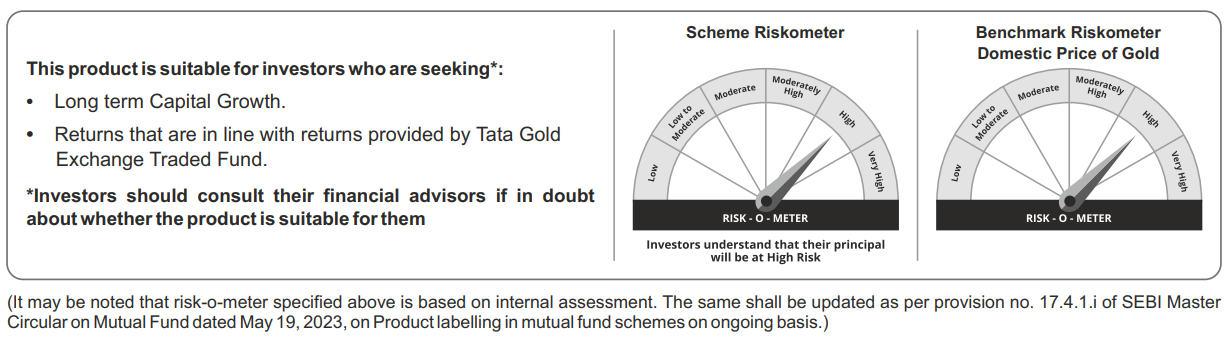

Key Terms – Tata Gold ETF

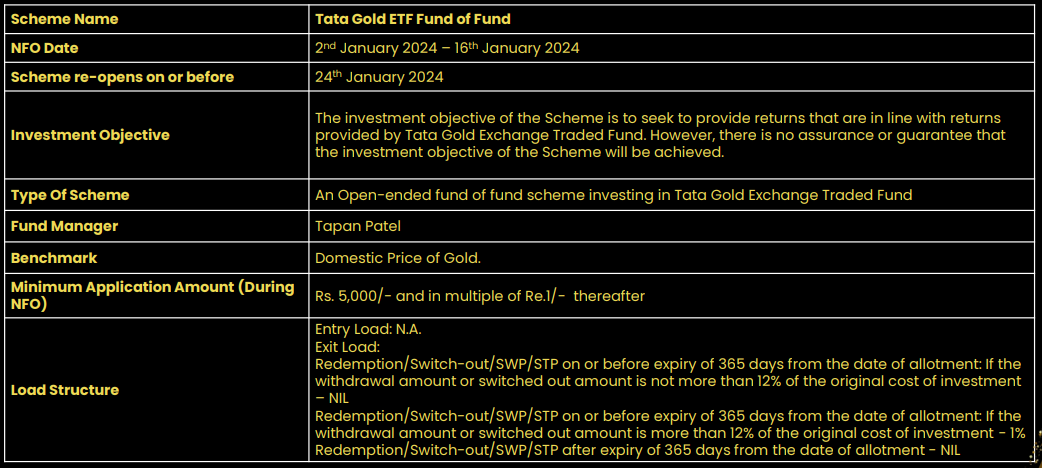

Key Terms – Tata Gold ETF FoF

Mutual Fund Investments are subject to market risks, read all Scheme related documents carefully.*

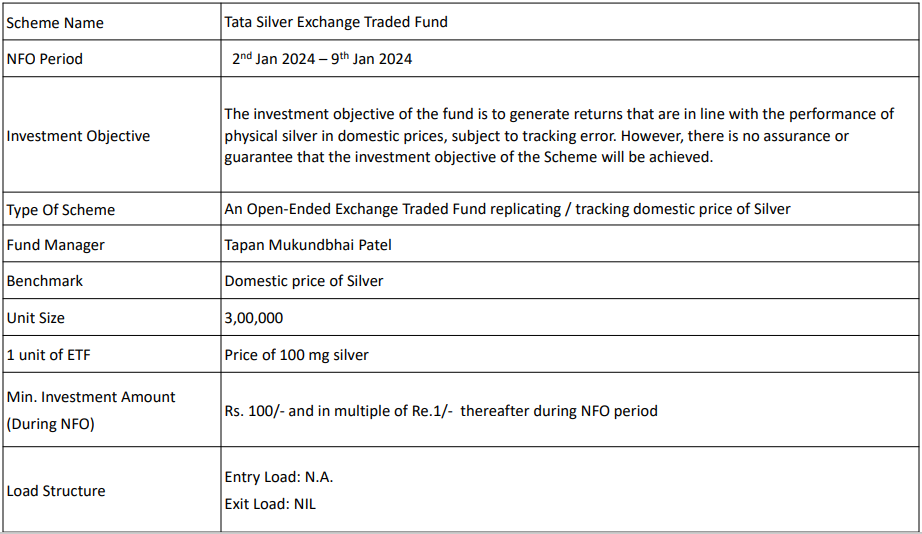

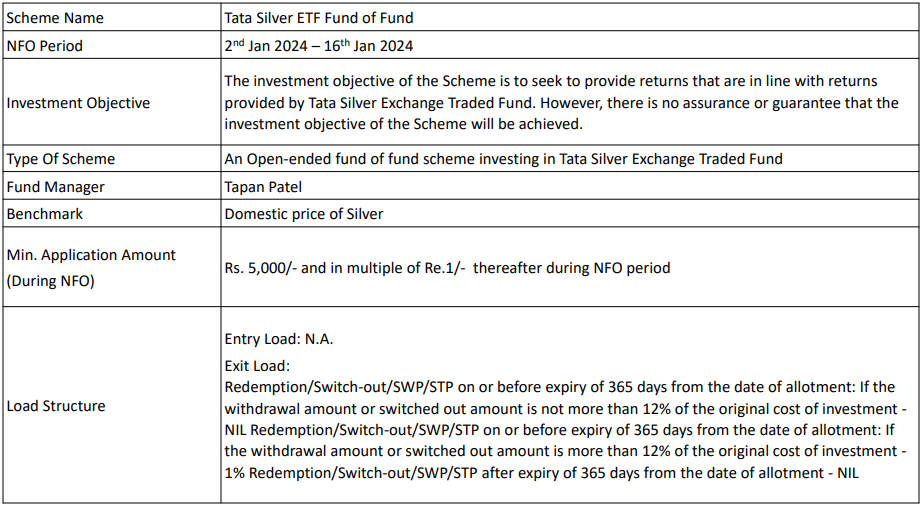

Tata Silver Exchange Traded Fund and Tata Silver ETF Fund of Fund

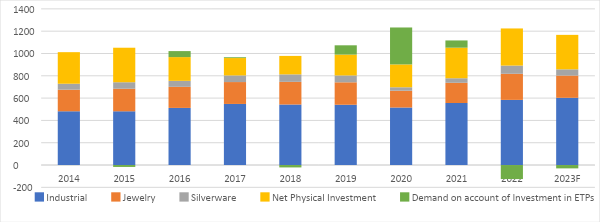

Silver as a commodity has the dual advantage of precious metals and industrial metal. Apart from traditional household usage, the use of Silver has been majorly dominated by industrial usage. The industrial usage lies in industrial batteries, manufacturing/textiles, solar panel, photography, mirror etc while the new era usage are EV, 5G technology, Bio pharma & medical, induction charges, green energy etc. Over the last few years, there has been a rise in demand for Silver which couldn’t be met by supply, leading to price rise. A major chunk of demand comes from industrial uses of Silver. Industrial demand for Silver has been on the rise since 2020.

Silver acts as an economic hedge during distress events and could tend to perform well along with gold during market uncertainty. In an economic growth scenario, demand for silver rises from industries with an increase in manufacturing activities.

Through investing into Tata Silver ETF and Tata Silver ETF FoF, one can capitalise and capture this rise in industrial demand and its probable benefit to silver prices.

Silver – Global demand Trends

A major chunk of demand comes from industrial uses of Silver

(Source: Silver Institute, World Silver Survey 2023)

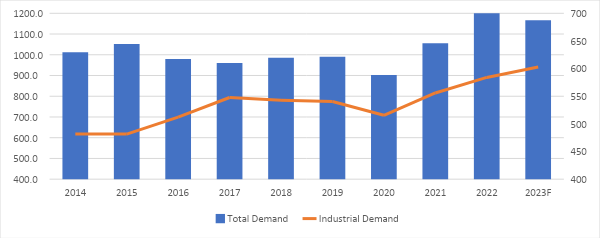

Silver – Total demand v/s Industrial demand

Silver – Total demand v/s Industrial demand

Industrial demand for Silver has been on the rise since 2020

(Source: Silver Institute, World Silver Survey 2023)

Key Terms – Tata Silver ETF

Key Terms – Tata Silver ETF FoF

Mutual Fund Investments are subject to market risks, read all Scheme related documents carefully.*

The Tata Asset Management philosophy is centred on seeking consistent, long-term results. Tata Asset Management aims at overall excellence, within the framework of transparent and rigorous risk controls. Consistency, flexibility, stability, and service are our key tenets.