Last Updated on Oct 14, 2021 by Aradhana Gotur

Every loan attracts an interest amount which is nothing but a charge taken by the lenders or financial institutions to help service the debt. Every EMI contains a portion that goes towards the repayment of interest as well as principal amounts. Despite paying the same rate of interest against the same loan amount for the same tenure, there can be considerable differences in the interest amount repaid by two persons.

This can be due to the different methods of interest calculation that different lenders may use. Primarily, the two methods of interest rate calculation are flat interest rate and reducing balance interest rate. Here is a detailed look into the two methods and the differences between them, along with an example each to better understand the liability attracted under both.

This article covers:

- Flat interest rate

- Reducing balance interest rate

- Differences between flat interest rate and reducing balance interest rate

- FAQs

Table of Contents

Flat interest rate

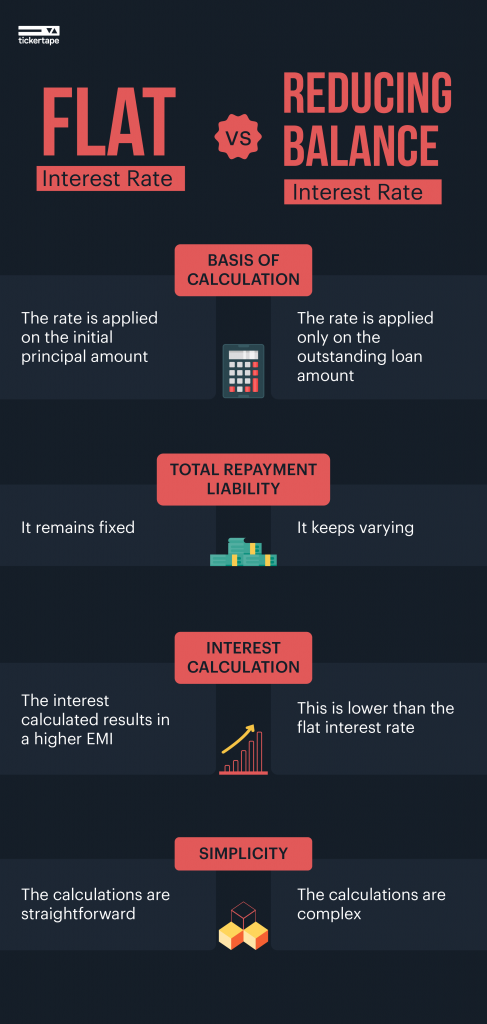

A flat interest rate involves calculating interest on the initial principal amount at the start of the tenure. The lending rate remains unchanged throughout. The total repayment liability remains fixed, which helps the borrower to plan his finances better. The interest calculation results in a higher EMI under the flat interest rate method. There are interest calculators available online for easy calculations. The formula for calculation of interest under this method is as follows:

For example, if you take a loan of Rs 2,00,000 for a tenure of three years, to be repaid at an interest rate of 10%. The interest component through the tenure would be Rs 60,000. When you divide principal plus interest by 36 mth, you get an EMI of Rs 7,222. By the end of the tenure, you would have paid Rs 2,60,000 in all.

Most personal loans and vehicle loans are calculated using a flat interest rate method. Since the interest is a fixed flat rate, the amount of interest paid does not decrease as the loan is repaid through the loan tenure. This is why this method is less popular amongst borrowers.

Reducing balance interest rate

Under the reducing balance interest method, the interest is calculated only on the principal amount outstanding at the end of a specific period. This means that the amount of interest accrued varies with the outstanding loan amount. The formula for calculating interest under the reducing balance method is as follows:

For example, if you take a loan of Rs 5,00,000 at an interest rate of 15% for a period of five years, the EMI here would be Rs 11,895 per month. Out of the total EMI paid in the first year of Rs 1,42,740, Rs 72,596 is the principal amount repaid and Rs 70,143 is the interest component. The principal balance amount that remains is Rs 4,27,404, on which the interest rate of 15% is calculated for the next EMI.

Because of this reason, this method is also known as the diminishing interest rate method. The total amount of interest the borrower ends up paying under this method is lower than that paid using the fixed interest method. This method is popularly used to calculate interest paid on housing loans, property loans, mortgages, overdraft facilities and so on.

Differences between flat interest rate and reduced balance interest rate

Following are some of the prominent differences between flat interest rate and reducing balance interest rate:

Calculation

The primary difference between the two methods is that the interest calculated in the flat interest rate method is on the initial principal amount sanctioned. In contrast, the interest calculation under the reducing balance interest rate is only on the outstanding loan amount.

Simplicity

The calculations are more straightforward in a flat interest rate method as compared to the reducing balance method.

Rates

The interest rates used in flat interest rates are generally lower than the reducing balance rate.

FAQs:

How is the interest rate decided?

The Reserve Bank of India sets the repo rate, which is nothing but the rate at which commercial banks borrow from RBI. Based on this repo rate, banks issue their lending rates.

How can I know my EMI before taking any loan?

The EMI should be calculated before taking any loan. It is better to understand a complete amortisation schedule for your loan based on the loan amount, tenure, and interest rate. This is possible via manual calculation. For ease of calculation, you can also refer to an EMI calculator available online for free.

Flat interest rate or reducing balance method, which is better?

This is a subjective decision that should be taken based on your financial requirements and repayment capacity. Overall, you will end up paying less interest under the reducing balance method, but the loan tenure is shorter as you will end up repaying the loan faster.

- Dolly Khanna Portfolio: Listed Stocks, Bulk and Block Deals, and Net Worth - Mar 4, 2026

- Best Performing Index Funds in India (2025) - Jun 5, 2025

- Issue of Shares – Meaning, Types, Examples and Steps - Jun 4, 2025