Last Updated on Dec 21, 2023 by Harshit Singh

Welcome to the December 2023 edition of Netra, where we explore a range of investment and economic trends. This issue covers the benefits of SIPs in small-cap stocks, analyses India’s economic growth post-liberalisation, examines the effects of China’s economic slowdown on India’s FDI, and assesses the recovery of India’s unorganised and rural economy. Additionally, we contrast the varying market trends in the US and India, providing key insights for investors.

The 5th edition of Netra can equip you with comprehensive knowledge to navigate the complex global economy.

Table of Contents

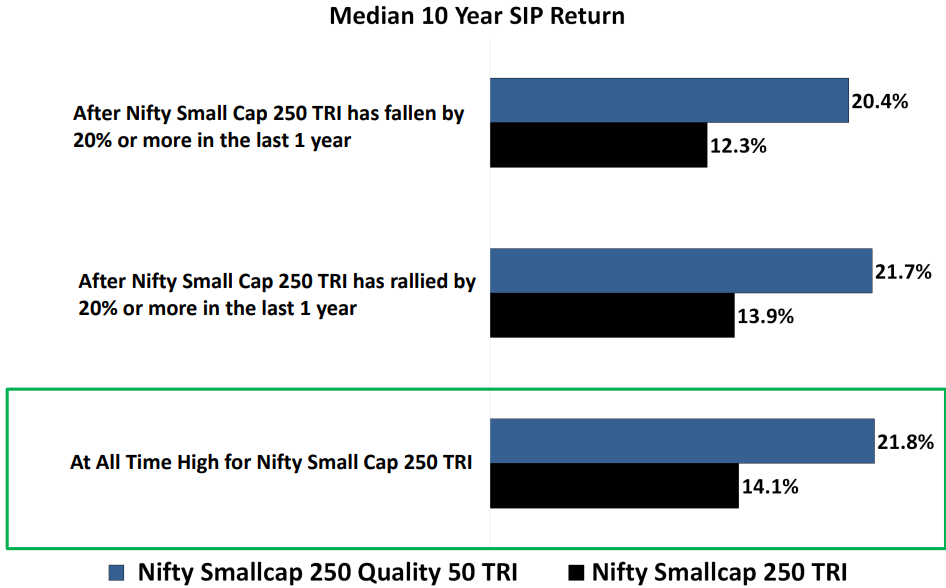

Navigating small cap investments: The strategic advantage of starting SIPs at market peaks

Investing in small-cap stocks can be a challenging yet rewarding endeavour, particularly in a fluctuating market landscape. The key to unlocking their potential lies in the timing and method of investment, with a Systematic Investment Plan emerging as a strategic tool, especially when initiated at market highs.

Source: Bloomberg, DSP; Data as on Nov 2023

Beginning an SIP when the market is at its peak might seem counterintuitive, but it offers a crucial behavioural advantage. Initial investments made at high prices often result in lower short-term returns. This phenomenon serves as a natural moderator of expectations, encouraging investors to adjust their return outlook and commit to a longer investment horizon. Such a mindset is vital in navigating the volatility inherent in small-cap investments.

A core principle of SIPs is that they allow investors to purchase more units of an investment when prices are lower. In the context of small caps, this means that when the market recedes from its peak, your SIP will enable you to accumulate a greater number of units at reduced prices (falling Net Asset Values or NAVs).

The accumulated units then stand to gain significantly from subsequent market upswings. As the market recovers and NAVs rise, these additional units multiply the benefits of increasing valuations. The equation is simple yet powerful: more units multiplied by a higher NAV equals greater wealth creation.

Investing in a Quality Index through an SIP, particularly during market peaks, has historically shown to yield consistent returns, irrespective of whether the market is at a peak or trough. This consistency outperforms broader indices, underscoring the importance of focusing on quality investments, especially when markets are priced high.

The right move with small caps

When small-cap indices hit all-time highs, the instinct might be to wait for a dip. However, history and strategy suggest otherwise. Starting an SIP in this scenario is not just a viable option but a recommended strategy. It provides a structured, disciplined path to potentially higher long-term gains alongside encouraging a focus on quality, fostering a healthy investment attitude, and optimising unit accumulation to maximise returns during market recoveries. It also mitigates the risks of timing the market and leverages the potential upside of small-cap volatility.

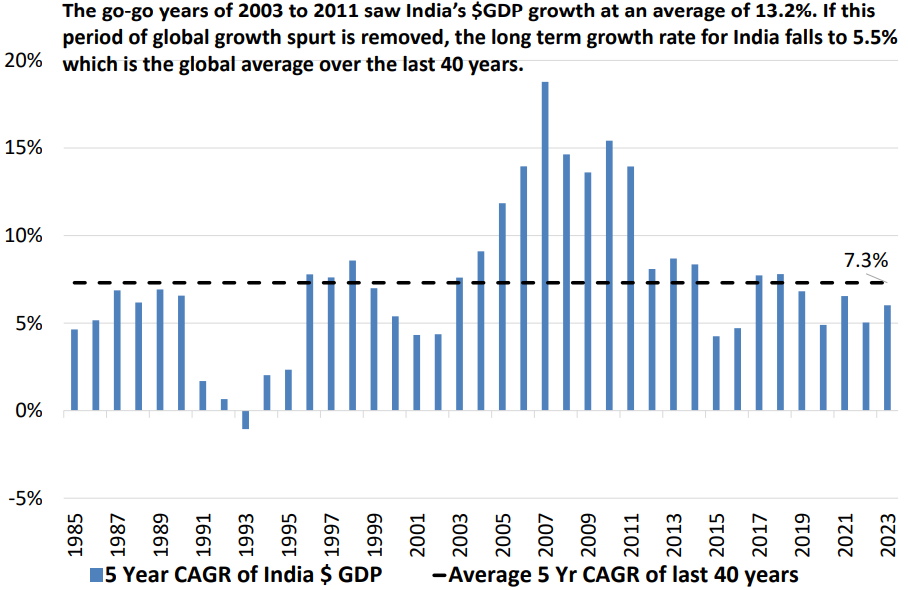

Decoding India’s economic growth: A journey from liberalisation to the present

India’s economic growth story is both impressive and multifaceted, marked by significant milestones and influenced by global economic trends. A closer look at the numbers offers a clearer understanding of this journey and its potential future trajectory.

Source: IMF, DSP; Data as on Nov 2023

The long-term growth rate

Since liberalisation in 1991, India’s Gross Domestic Product (GDP) has grown at an impressive average of 7.5%. This accelerated growth post-liberalization marks a notable shift from the previous long-term average of 7.3%.

With a Compound Annual Growth Rate (CAGR) of 7.2%, India’s economy has shown the potential to double in size approximately every 10 years. This exponential growth trajectory suggests that barring unforeseen circumstances, India’s current GDP of around $3.5 trillion could potentially expand to $7 trillion by 2032.

The period between 2003 and 2011, also known as the Boom Years stands out as the zenith of India’s economic growth, with an average GDP growth rate of 13.2%. However, it’s crucial to contextualise this within the global economic landscape, where the world GDP was also growing robustly at an average of 7.6% – surpassing its long-term average of 5.5%.

The crucial insights one can draw from this data

India’s economic fortunes have historically been closely tied to the global economic climate. A thriving global economy often translates into tailwinds that propel India’s growth.

Also, as India’s economic base has expanded, maintaining high growth rates has become more challenging. The era of achieving 7% or higher growth rates was facilitated by a smaller economic base, buoyed by a large population and favourable global conditions.

Today, the global economic landscape is more fragmented, posing significant headwinds to India’s growth trajectory. The concept of ‘decoupling’ – India’s economy growing independently of global trends – remains more of a theoretical construct than a practical reality at this stage. For investors and policymakers alike, this understanding is key to making informed decisions in a rapidly evolving economic environment.

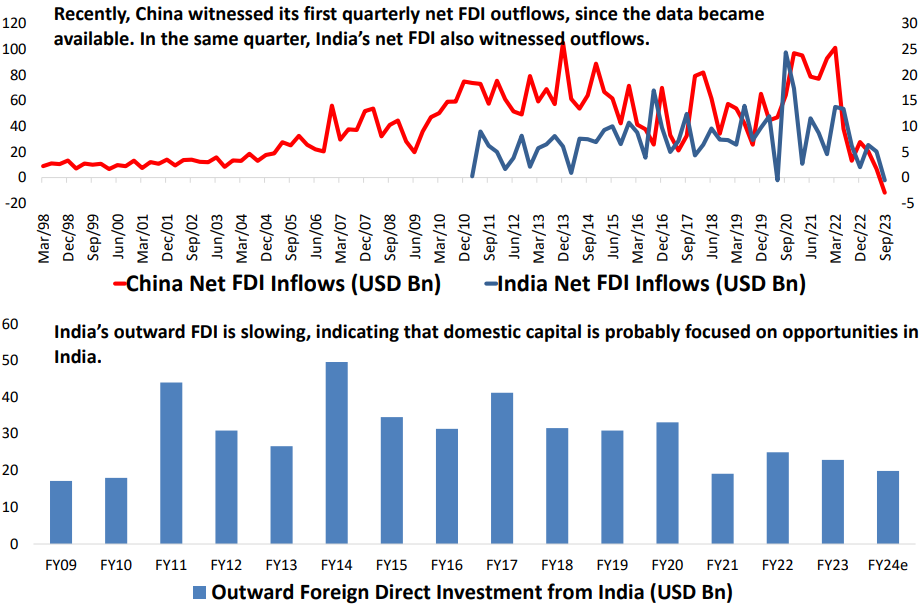

Assessing India’s position in the wake of China’s economic slowdown: A closer look at FDI trends

The global economic landscape is experiencing shifts, with significant changes in investment flows, particularly in the context of China’s growth slowdown. Understanding how these shifts affect India’s ability to attract Foreign Direct Investment (FDI) is crucial in gauging the country’s standing in the global economy.

Source: Bloomberg, DSP; Data as on Nov 2023

The current state of global FDI

For the first time since record-keeping began in 1998, China experienced a net FDI outflow of $11 billion in September 2023. This marks a significant shift in global investment patterns, given China’s longstanding role as a major FDI recipient.

Similarly, India witnessed a net outflow of $537 million in the same quarter, only the second instance of such an outflow since data collection started in 2012. This trend challenges the narrative that India might be capturing the FDI diverted from China.

The assumption that India would automatically benefit from China’s economic slowdown by attracting foreign investments is yet to be substantiated by the numbers. All emerging markets are navigating these turbulent waters, but their success in attracting FDI depends on individual country circumstances, policy environments, and economic stability.

The global investment climate is becoming increasingly cautious, with foreign capital becoming scarce. This is evident in the cumulative Foreign Portfolio Investment (FPI) flows over the past two years, which show net outflows from both India and China. FPI, often referred to as ‘hot money’, is indicative of the short-term investment sentiment towards a country’s stock markets.

The broader economic implications

These trends reinforce the idea that India’s economic fortunes are closely linked to global economic health. A thriving global economy tends to favour India, whereas a global slowdown can adversely impact its ability to attract foreign investments.

For India to capitalise on any potential FDI shifts resulting from China’s slowdown, it would require not just favourable global conditions but also proactive policy measures, improved ease of doing business, and political stability.

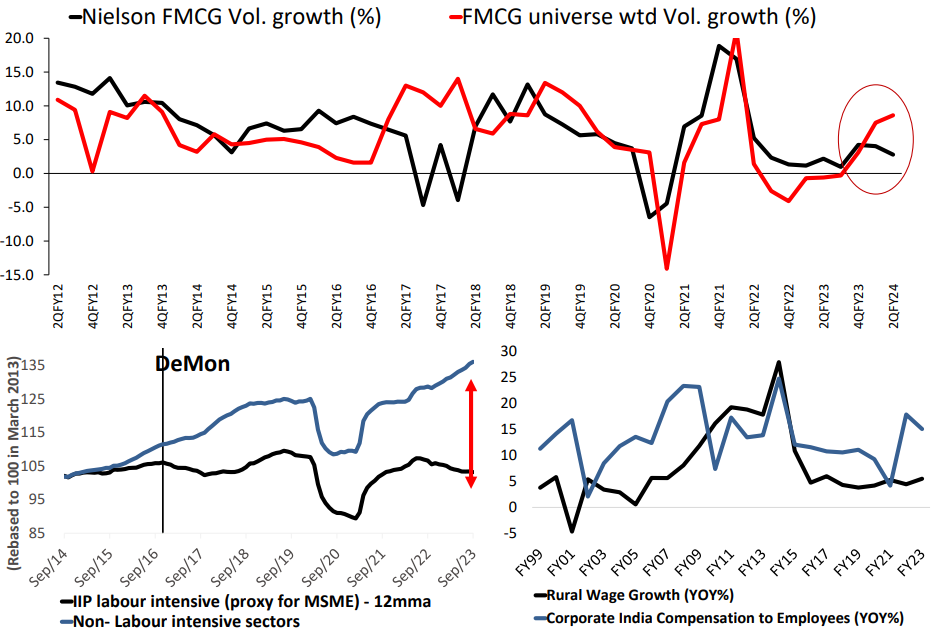

Exploring the resilience of India’s unorganised and rural economy in the Post-COVID era

The unorganised and rural sectors in India have faced significant challenges in the wake of the COVID-19 pandemic. However, recent developments suggest a potential turnaround. Below is the current state of these sectors and the indicators pointing towards a possible recovery.

Source: Bloomberg, DSP; Data as on Nov 2023

India’s economic rebound from COVID-19 has been uneven, with the rural and unorganised sectors particularly struggling. These segments have grappled with multiple setbacks, including the initial shock of the pandemic, a sluggish employment recovery, and the brunt of high inflation in 2022 and the first quarter of 2023.

The industrial production data, often used as a proxy for the Micro, Small, and Medium Enterprises (MSME) sector—which is labour-intensive and largely unorganised—has yet to show a significant recovery. This indicates that the upturn in these sectors might still be in the nascent stages.

The listed Fast-Moving Consumer Goods (FMCG) universe is beginning to show an increase in volume growth, and the industry commentary is becoming increasingly supportive of a recovery. This trend, if corroborated by hard data, could signal the start of a steady recovery trend. It also has significant implications for sectors closely linked with rural and unorganised market segments, such as FMCG and automobiles.

While these early signs of recovery in the unorganised and rural sectors are encouraging, a cautious approach is warranted until these trends are more clearly reflected in economic data. A confirmed upswing in these sectors could have far-reaching implications. It could signal a broader economic recovery and provide investment opportunities in sectors that cater to or are influenced by the unorganised and rural markets.

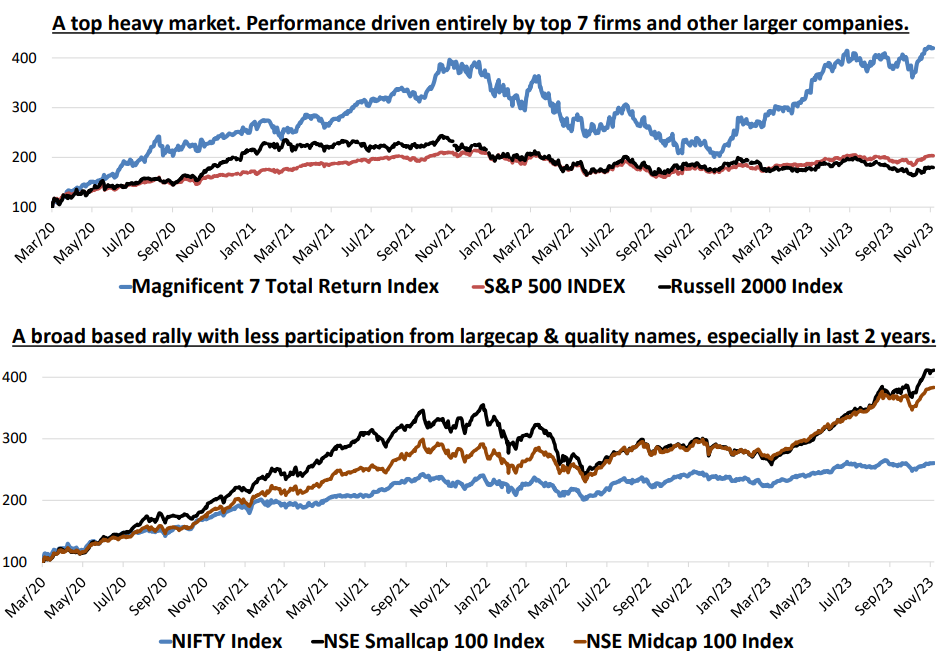

The tale of two markets: Dissecting divergent trends in US and Indian stock markets

The dynamics of the stock markets in the US and India present a stark contrast in terms of market concentration and the performance of different segments. Understanding these differences is key to comprehending the broader implications for investors and the health of these markets.

Source: Bloomberg, DSP; Data as on Nov 2023

The US market

In the US, the stock market has become increasingly concentrated. The ‘magnificent seven’ – Apple, Microsoft, Amazon, Alphabet, Meta Platforms, Nvidia, and Tesla – represent a substantial portion of the overall market capitalization. This concentration has significant implications for market dynamics and investor strategies.

Despite challenges in growth, these large companies have been pivotal in sustaining the US equity market. Their performance has often masked underlying weaknesses in the broader market.

On the other hand, the broader small and mid-cap stocks in the US have not fared as well, languishing at multi-month lows. This divergence indicates a market that is increasingly dependent on a few large players, a situation often viewed as unhealthy, especially when broader economic support is lacking.

The Indian market

Contrary to the US, the Indian stock market has seen its smaller and mid-cap stocks outperform large-cap ones by a significant margin. This trend is reflective of a broader economic revival and optimistic earnings growth prospects across market caps.

This resurgence in the broader Indian economy has played a crucial role in buoying these segments of the market. This diversified growth is a healthy sign, indicating a more robust and inclusive market recovery.

However, this rally in India is not without its risks. The growth outlook, which is closely linked to corporate earnings growth, remains a critical factor. There’s a possibility that normalisation in growth could impact the performance of the wider market, suggesting a need for conservative investment strategies.

Implications for investors

In the US, investors need to be mindful of the over-reliance on a few large companies. Diversifying investments beyond these blue-chip names could be prudent, especially considering the weak performance of the broader market.

For those looking at the Indian market, the current scenario presents opportunities across various market caps. However, vigilance regarding economic indicators and earnings growth is essential to navigate potential volatility.

The bottom line

As we conclude this December 2023 edition of Netra, it’s clear that the realms of investing and economic development are laden with complexities. From the strategic use of SIPs in small-cap investments during market highs to the impact of global economies on FDI flows, the landscape is ever-changing. India’s robust economic growth story paints a picture of resilience and adaptability. Meanwhile, the contrasting market dynamics in the US and India offer a stark reminder of the diversity in investment landscapes. These insights underscore the importance of a well-informed, adaptive approach to investment and economic strategy.

Netra aims to provide not just analysis but actionable intelligence that can enable informed decisions amidst constantly evolving economic narratives. Access the full report here for more insights.

Disclaimer

Past performance may or may not be sustained in the future and should not be used as a basis for comparison with other investments. There is no assurance of any returns/capital protection/capital guarantee to the investors in this scheme of DSP Mutual Fund. This note is for information purposes only. In this material, DSP Asset Managers Pvt Ltd (the AMC) has used information that is publicly available and is believed to be from reliable sources. While utmost care has been exercised, the author or the AMC does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers, before acting on any information herein should make their own investigation & seek appropriate professional advice. All opinions/ figures/ charts/ graphs are as of the date of publishing (or as at the mentioned date) and are subject to change without notice.

Large-caps are defined as top 100 stocks on market capitalization, mid-caps as 101-250, small-caps as 251 and above. Data provided is as on October 31st, 2023 (unless otherwise specified). It is not possible to invest directly in an index. For complete details on investment objective, investment strategy, asset allocation, scheme specific risk factors and more details, please read the Scheme Information Document, itStatement of Additional Information and Key Information Memorandum of the scheme available on ISC of AMC also available on www.dspim.com. Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implications or consequences of subscribing to the units of the schemes of DSP Mutual Fund. The statements contained herein may include statements of future expectations and other forward looking statements that are based on prevailing market conditions / various other factors and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. The recipient(s) before acting on any information herein should make his/their own investigation and seek appropriate professional advice.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

- Netra April 2024 Market Analysis Report – 3 Key Takeaways! - Apr 26, 2024

- Netra March 2024 Market Analysis Report – 3 Key Takeaways! - Mar 20, 2024

- Trading Actively? You Need “Something Just Like This” - Mar 15, 2024