Last Updated on Dec 5, 2024 by Harshit Singh

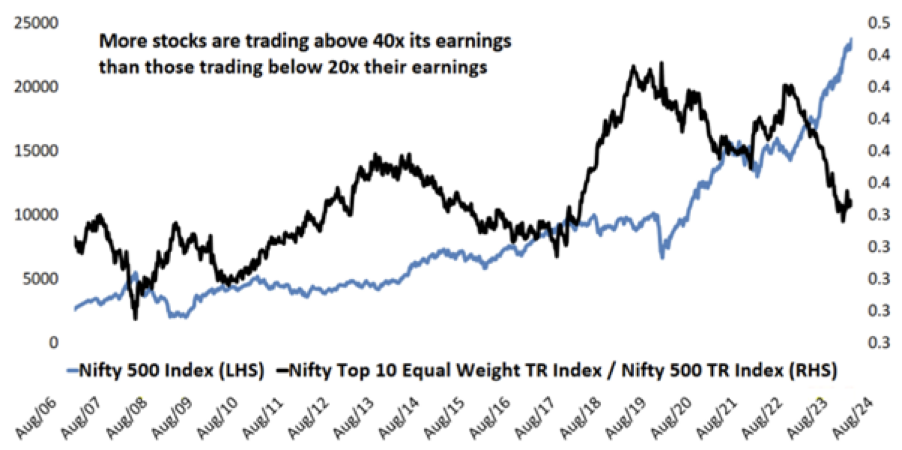

The largest of the large caps: we’ve talked about them several times in the recent past, and for good reason. These stocks have perhaps never had it so bad before. Not only has their weight in the total market capitalisation dwindled to an all-time low, but their relative price performance also hit an all-time low recently. This latter point can be observed in the chart below.

This spell of underperformance from the very biggest stocks might represent an excellent opportunity for investors, simply because a regression to the mean from this point is quite possible.

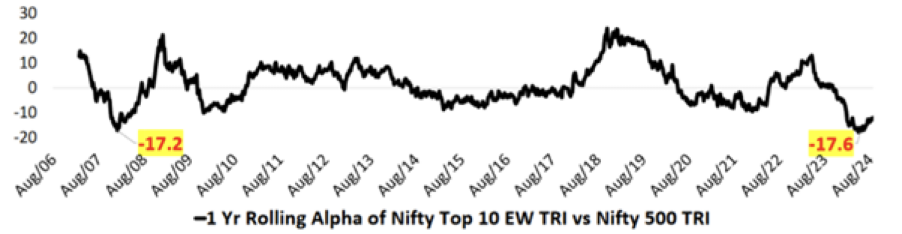

Consider the chart below, which plots the 1-year rolling alpha (i.e. outperformance) of the Nifty Top 10 Equal Weight index relative to the Nifty 500. Notice how the rolling alpha bounced back during 2007-08, when the rolling alpha was roughly as low as it currently is.

Moreover, the large addition to India’s overall equity market capitalisation from new listings has made the top 10 cohort even more attractive. This is because more than two-thirds of these new issues were listed at prices that were greater than 50x of their trailing earnings. As a result, this newly infused market cap component has a low profitability base when compared to the top 10 stocks.

Historically, periods of inflection in the underperformance of the 10 largest-cap stocks versus the rest of the market have coincided with a general ‘risk-off’ environment, i.e. during such times, investors have usually been especially keen on reducing their risk exposure and protecting their capital. Given recent concerns that the small- and mid-cap (SMID) category might be too frothy and overvalued, it’s possible that such a risk-off environment might be on the horizon.

Lastly, it’s important to note that on an absolute basis, even the top 10 stocks aren’t currently cheap from a historical perspective. Hence, they should be looked upon as a relative play for investors looking to add some equity exposure.

Table of Contents

Time to mine value from mining?

Gold is up 20% this year thanks to a variety of reasons, including inflation and safe-haven demand. This recent strength in gold prices, coupled with operational improvements, has increased the valuation appeal of the gold mining sector.

Historically, it has been seen that gold mining stocks go up in price after gold rallies. While both gold mining companies and gold have underperformed stocks for most of the last decade1, some positive changes have been noted over the past few years.

After Covid, several gold mining companies got rerated, and their balance sheets started to get cleaner. Companies in this sector are now carrying out more disciplined capex. In addition, more stable oil prices have contributed to a fair degree of margin expansion, and gold mining companies are paying back decent amounts to shareholders in the form of dividends and buybacks1.

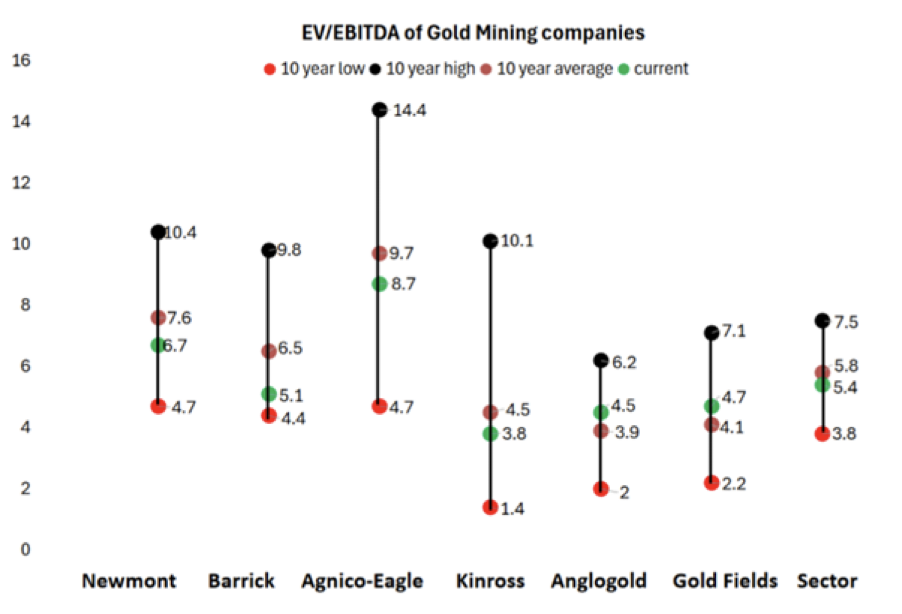

Best of all, gold mining stocks have gotten relatively cheaper: currently, the sector is trading below its 10-year average valuations (as measured using the ratio of the enterprise value EV to the EBITDA), offering potential opportunities for investors.

Key players in the gold mining industry — chiefly Newmont, Barrick, and Agnico-Eagle — are trading at valuations that are significantly below their historical norms. This is largely due to their stronger balance sheets and enhanced operational efficiencies, making them particularly attractive investments at these levels.

Historically, there has been a valuation gap between senior gold miners, such as Newmont, Barrick, and Agnico-Eagle, and their smaller counterparts, including Kinross, AngloGold, and Gold Fields. However, this dynamic could be poised for a change.

The smaller mining companies could see a valuation rerating, driven by their robust operational performance, healthy cash flows, and growth potential, which are supported by higher gold prices. Mergers and acquisitions could also strengthen smaller mining companies; for instance, AngloGold recently agreed to acquire Centamin, Egypt’s largest gold miner, for $2.5 billion. This deal, once finalised, should boost AngloGold’s production by around 450,000 ounces per year.

1 Source: DSP

Shifting gears on the market cycle

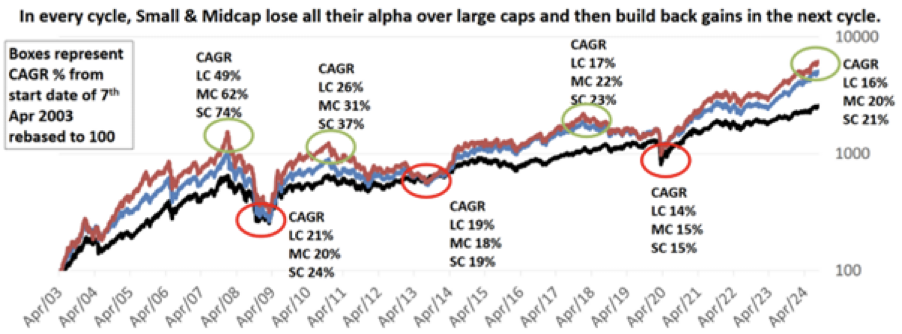

The Indian stock market moves in cycles. During each upcycle, relatively small firms from the small- and mid-cap (SMID) space exhibit stellar performance. As can be seen in the chart below, SMID stocks have significantly outperformed large caps (LCs) in every upcycle bull market so far.

What the above chart also reveals is that during each downcycle, SMID stocks lose almost all the alpha (i.e. outperformance) generated during the previous upcycle. This is consistent with the typical volatility that SMID stocks exhibit: their relatively higher volatility results in larger drawdowns during bear markets compared to the relatively shallow declines seen among large caps.

What does this mean for investors? Capturing the extra alpha that SMID stocks can deliver requires investors to focus on the margin of safety (i.e. the gap between a stock’s market price and its intrinsic value) rather than relying on recent outperformance.

In fact, it makes a lot of sense to have an aggressive attitude towards SMID stocks when their alpha over large caps is low. Currently, SMID stocks have a large alpha over large caps, so investors might be better served by focusing more on large caps.

For more actionable insights backed by data and analyses, we invite you to read the latest edition of Netra in its entirety.

Disclaimer

This document is for information purposes only. The recipient of this material should consult an investment /tax advisor before making an investment decision. In this material DSP Asset Managers Pvt. Ltd. (the AMC) has used information that is publicly available, including information developed in-house and is believed to be from reliable sources. The AMC nor any person connected does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Data provided is as on December 31, 2023 (unless otherwise specified and are subject to change without notice). Past performance may or may not be sustained in the future and should not be used as a basis for comparison with other investments. There is no assurance of any returns/capital protection/capital guarantee to the investors in above mentioned scheme. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information document of the scheme. The statements contained herein may include statements of future expectations and other forward-looking statements that are based on prevailing market conditions / various other factors and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements.. The sector(s)/stock(s)/issuer(s) mentioned herein do not constitute any research report/recommendation of the same and the scheme/ Fund may or may not have any future position in these sector(s)/stock(s)/issuer(s). The strategy / investment approach / framework mentioned herein is currently followed by the scheme and the same may change in future depending on market conditions and other factors.

For complete details on investment objective, investment strategy, asset allocation, scheme specific risk factors and more details, please read the Scheme Information Document, and Key Information Memorandum of the scheme available on ISC of AMC and also available on www.dspim.com. For Index disclaimer click here. Large-caps are defined as top 100 stocks on market capitalization, mid-caps as 101-250 , small-caps as 251 and above. The strategy mentioned has been currently followed by the Scheme and the same may change in future depending on market conditions and other factors.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

– A Smart Alternative to Gold Exposure")