Last Updated on Sep 13, 2022 by Aradhana Gotur

At BSE, Muhurat Trading has been over a 60-yr-old tradition. It continues to have a deep emotional connection with the investor community, especially those who have been in the markets for a few decades. Now that we are just two days away from the one-hour long trading session, we asked two smallcase managers—Ambareesh Baliga and Ekansh Mittal—the stocks and sectors in their watchlist for the special trading session.

Let’s take a look.

Table of Contents

Ambareesh Baliga‘s picks

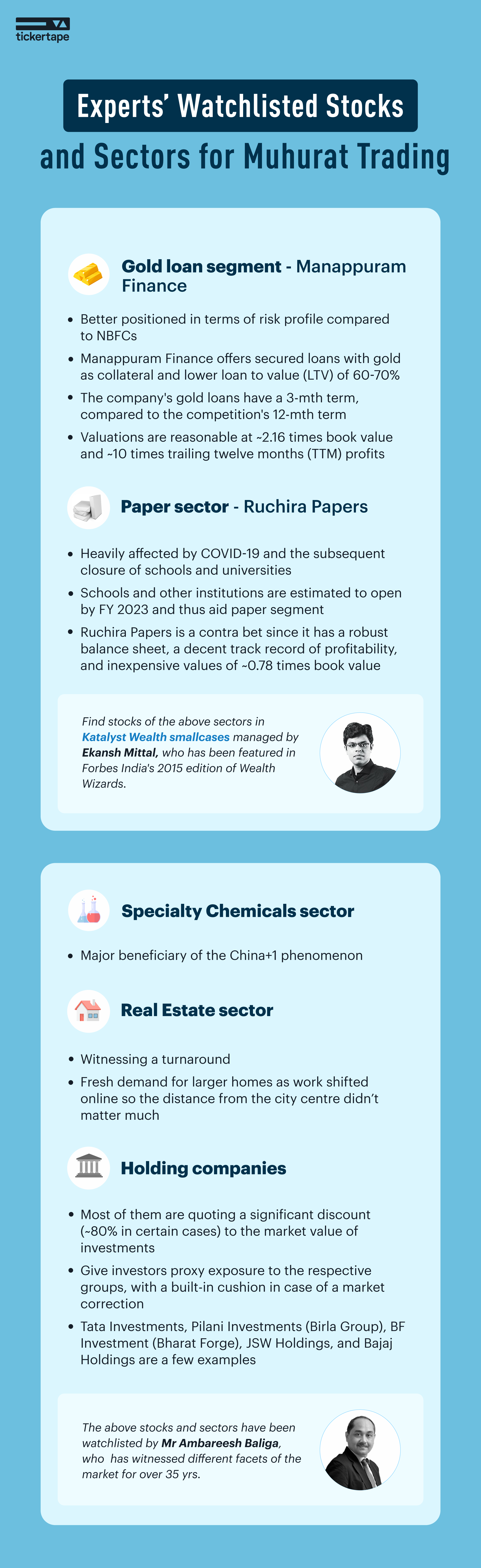

Mr Ambareesh Baliga, is experienced in different facets of the market for over last 35 years and has been acknowledged for his acumen and understanding of the stock markets.

Specialty Chemicals sector

Among the various sectors, Specialty Chemicals would continue to be the major beneficiary of the China+1 phenomenon, but most of the market leaders are extremely expensive and are discounting the best growth opportunities. Automobiles, despite lower offtake, have been betting on the chip shortage issue to be sorted out soon. After a bout of underperformance, the sector was charged and backed by Tata Motors.

Real Estate sector

Real Estate seems to be witnessing a genuine turnaround and many analysts and investors are still in disbelief as this sector was off the radar for many years. The sector has been struggling for the last over 7 yrs with many developers defaulting on loans. Every major policy change of the government affected them initially. Demonetization changed the way they did the business. ReRa brought in regulations that were a 180-degree transformation. GST on Real Estate was confusing even for the government which changed it several times within a year of introduction. And last but not the least, the COVID-19 pandemic was expected to be the death knell for this sector.

However, contrary to the expectations, the pandemic created fresh demand for larger homes and the distance from the city centre didn’t matter much as work shifted online, and so did the shopping experience. When most of the daily routine was online, one needed a better living environment. A country like India, with decently high population growth, has also been witnessing nuclearization of the families. Though this has been leading to increased demand for housing for decades, the demand had turned ‘latent’ in the last few years as many were waiting for lower levels, thus turning ‘fence sitters’.

Most of these fence sitters jumped into the fray as the government introduced sops to boost the demand. Along with this, the increase in input costs ensured that new projects were launched at higher prices than the existing projects, thus the price uptick too ensured the urgency to close deals. With no further price correction, the demand continues to improve despite the withdrawal of various sops, confirming a long term uptrend.

Check out smallcases by Ambareesh Baliga.

Though some of the leaders have become multibaggers in the last year, we should possibly wait for a correction to buy into this sector that has a good potential for the foreseeable 4-5 yrs.

Holding companies

Another segment – though can’t be strictly termed a sector – are holding companies. These are investment companies of large groups holding a large chunk of the promoter families. For example, Tata Investments, Pilani Investments (Birla Group), BF Investment (Bharat Forge), JSW Holding, Bajaj Holdings, Bombay Burmah (Nusli Wadia) and the likes. Most of them are quoting a huge discount (as high as 80% in a few cases) to the market value of their investments. These holding companies provide the investor proxy exposure to the respective groups with a built-in cushion in case of a market correction.

“Though I am not an aggressive buyer in this market, the above two segments/sectors would be on my radar for the ensuing Samvat.” says Ambareesh.

Ekansh Mittal

Ekansh Mittal is the founder of Katalyst Wealth, who started investing in stocks at the age of 21 and has been featured in Forbes India’s 2015 edition of Wealth Wizards and Economic Times (ET) May 2017 edition of Dons of Dalal Street. Mr Ambareesh Baliga, is experienced in different facets of the market for over the last 35 yrs and has been acknowledged for his acumen and understanding of the stock markets.

We like the following sectors and stocks from a perspective of 2-3 yrs and create a watchlist for Muhurat Trading.

Gold loan segment

Gold loan companies are basically a part of a larger group of NBFCs; however, they are relatively much better placed in terms of risk profile.

Unlike other NBFCs where one isn’t exactly sure of the assets profile of the company, in the case of gold loan companies, they give out secured loans with gold holdings of the borrower as collateral and lower LTVs of 60-70%. The loan duration is 3-12 mth and therefore the risk of loss is very low with such loans. (Continues after the infographic)

Around a year back, gold prices had started rising and with lower opportunities for lending in other segments, a lot of NBFCs and banks jumped into the arena of gold loans. Even the RBI had relaxed the LTV norms for banks to 90% till March 2021.

Since then, the gold prices have corrected by ~20% and the new players including the banks will face the heat on account of both higher LTVs and aggressive disbursal at higher gold prices.

On the other hand, Manappuram Finance’s gold loans are of short tenure of 3 mth against around 12 mth for the competition. Thus, the company is far ahead of the competition in managing the price risk.

Besides gold loans, the company is also present in the segments of microfinance, home loans, and CV finance.

The gold loan business continues to be the foundation of the company and should resume the growth trajectory with the closure of higher LTV loans and stable gold prices. The management has shared the guidance of 10-15% growth assuming stable prices. For other verticals, they are aiming for ~20% growth.

Given the above-mentioned factors, we believe the valuations are reasonable at around 2.16 times book value and around 10 times TTM earnings (last 12 mth earnings).

Paper sector

Paper sector got badly impacted on account of COVID-19 and the resultant shut down of schools and colleges and online teaching.

Schools and other institutions have started opening and we believe from FY 2023 all the institutions will be opened and the students will start going back to schools and colleges.

This should augur well for the writing and printing paper segment and the companies with strong balance sheets from the sector.

As a result, we like Ruchira Papers as a contra bet which has a good history of performance, a strong balance sheet and low valuations at around 0.78 times book value.

For Ruchira, the 7 yrs average PAT is Rs. 25 cr. and the average cash flows from operations (after deducting interest and adding back other income) for the last 7 yrs is Rs. 29 cr. against the current market cap of Rs. 208 cr.

Overall, qualitatively, the company has done well over the years. We also believe the bad phase will turn around with gradual improvement in profitability in the quarters ahead.

You can check out Katalyst Wealth smallcases.

With all this in place, let’s now prepare for Diwali with a portfolio ready approach with Muhurat Trading in mind.

Disclosure: Ekansh is a SEBI Registered Research Analyst (Registration No. INH100001690). Manappuram Finance and Ruchira Papers have been recommended to clients and he has a personal investment in Manappuram Finance.

Disclaimer: This article is only for informational purposes and should not be construed as investment advice, suggestions or recommendations. Do your own research or consult a financial advisor before investing.

- Dolly Khanna Portfolio: Listed Stocks, Bulk and Block Deals, and Net Worth - Mar 4, 2026

- Best Performing Index Funds in India (2025) - Jun 5, 2025

- Issue of Shares – Meaning, Types, Examples and Steps - Jun 4, 2025