: What You Need To Know")

Last Updated on Sep 20, 2023 by Anjali Chourasiya

Last week, the Wholesale Price Index (WPI) suggested that, on average, wholesale prices in India have contracted by 0.5% in the month of August 2023 compared to the same month last year. On the other hand, the Consumer Price Index (CPI) suggested a price increase of 7% year-on-year (y-o-y). So, how do we navigate this information? Let us start with the basics.

CPI vs WPI

If we go down the supply chain from manufacturer to retailer and then to the final consumer, then the CPI gets calculated at our level, i.e. the last price paid by consumers while the WPI comes into the picture before the distribution phase. There is another major difference between them, and that is the inclusion of the services sector. CPI includes prices of services like hospital fees, hotel fares, school fees, and so on and so forth. The WPI does not include any services. However, such a method is peculiar to India. Many countries use the producer’s price index (PPI), which includes wholesale prices of both goods and services.

The other aspect that creates difference is the component of both inflation measures. CPI focuses on consumers, and thus, food has a majority weightage at ~46%, while manufactured products account for 64% of WPI. Sometimes, the prices of only a few products change, like tomatoes. The weightage of tomatoes in CPI is 0.57%, while in WPI, it is 0.28%. Due to these three reasons discussed above, changes in prices of various things around us will have different effects on aggregate CPI/WPI. You can see that they do not go hand in hand most of the time in Figure 1 below.

The WPI Trend

WPI is influenced by the trend in prices of manufactured products because of its higher weightage. You can see a clear relationship in Figure 2. We can also see that wholesale food prices do not move in tandem with general WPI and manufactured products. In the last few months, we have seen an increase in food inflation. However, a decline in the prices of manufactured products has pulled the aggregate WPI down.

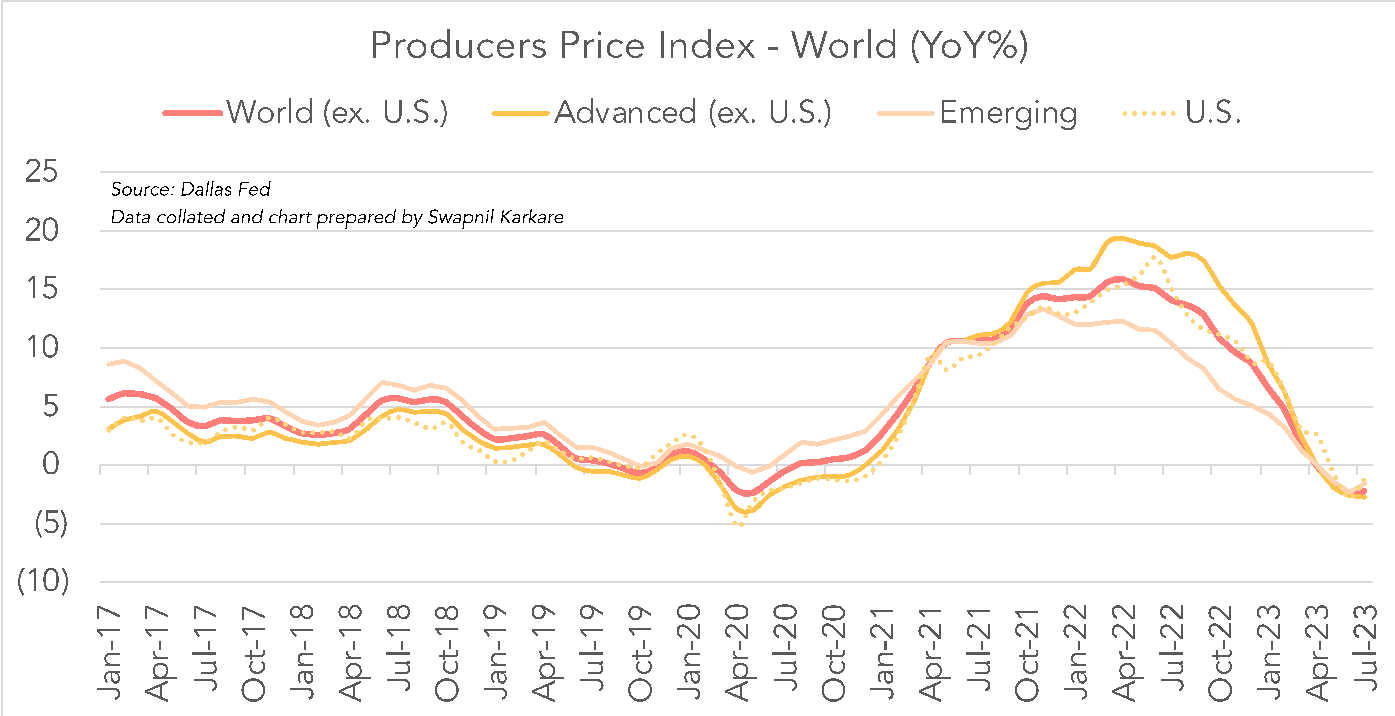

The ebb and flow of wholesale prices have been similar around the world (Figure 3). Commodity prices play a major role in driving wholesale prices. India’s WPI is highly correlated with the commodity index published by the World Bank (Figure 4). Over the last year, international commodity prices have been falling, putting downward pressure on raw material prices.

A lot of factors have contributed to the fall in commodity prices. Fear of recession (soft or hard landing – any) in the US, a slowdown in Europe and a sluggish economic recovery in China have curtailed overall demand for goods and services at a global level. If the manufacturers do not foresee a rise in demand, they will curb raw material sourcing, which will mean that the supply has to be adjusted with the reduced demand, which will again pull the prices down.

A negative WPI, however, is a consequence of a sluggish demand. The ideal scenario is to have WPI in positive territory. Positive inflation suggests that the economy is growing due to rising demand for goods and services. Although RBI has a mandate to control CPI at 4% with a margin of +/-2%, there is no such floor or cap for WPI.

Negative WPI

Wholesale prices or producer prices (whatever you call them) tell us two things: One, how will consumer prices move in the short term? Two, the health of the economy.

From the current trend of wholesale prices, we can say that over a few months, this decline in prices will be reflected in consumer prices, too. Low consumer prices will also impact central banks’ monetary policies. They might halt interest rate hikes for some time.

Lower wholesale prices mean that manufacturers do not enjoy pricing power. Sluggish or moderate growth within India and abroad suggests a reduction in aggregate demand in the economy. Due to lower demand, manufacturers are not able to raise prices. This suggests that they might offer discounts before the festive season to increase product demand. In case consumers respond to this positively and if the demand sustains, then we can see an uptrend in WPI.

But watch out for crude oil prices. Brent crude and WTI crude futures prices have surpassed US$90 per barrel. We have already seen in Figure 4 that WPI and commodity prices (including energy prices) move hand in hand. Commodity analysts from Bank of America and StanChart have not ruled out oil prices touching US$100. If that happens, WPI may turn positive, but during that period, the CPI can go beyond the acceptable levels, which can impact fiscal and monetary policies. It is believed that the next couple of quarters will be crucial for the global economy as many economies might fall into recession, and thus, we must keep an eye on inflation levels.

The key takeaways are: First, a positive WPI is a good sign for the economy. Second, a positive WPI but a very high CPI does not give us any relief as central banks track CPI for setting their monetary policies. Higher CPI means higher interest rates, entailing higher lending rates. Third, demand revival is the key to taking economies out of stagnation.

So, let us pray that everyone is happier and more prosperous this festive season and that we continue to spend more to keep the economy intact.

- Senior Citizens To Get Health Insurance? Facts Explained! - Apr 30, 2024

- How Stock Markets React to Interim Budgets: Cues From the History - Jan 31, 2024

- Top 5 Indian Economics Newsletters to Subscribe in 2024 - Dec 6, 2023