Last Updated on Jan 31, 2024 by Anjali Chourasiya

This time it’s different.

Every five years, the budget’s scope and nature change. Why? Because the government does not present a full-fledged budget.

As we approach Union Budget 2024, we must understand the basics of government functioning. Let’s also understand how stock markets react to such budgets.

Table of Contents

How is an Interim Budget different from a full-fledged budget?

There are elections in May 2024. That means a new government will come to power in the second or third month of the next financial year (i.e. FY 2024-2025). But how will the country function until the new government is formed? An interim budget solves this problem.

The primary objective of an interim budget is to address the government’s immediate expenditures for the initial months, ensuring continuity without disrupting essential services. It’s worth noting that, despite covering only the first few months, the government presents data, including allocations for schemes and programs for the entire year.

Commonly referred to as a ‘vote on account,’ the parliament approves the interim budget and permits the government to spend without the need for a detailed budget. Consequently, the current budget will not undergo parliamentary scrutiny. However, the next budget, due in July or August, will have to follow all the rules.

An intriguing question arises: Can the government leverage the budget to appeal to voters?

Well, the Election Commission discourages big bang reforms to prevent the politicisation of budgets. However, finance ministers craft their speeches giving a positive narrative of their governments’ achievements.

In a full-fledged budget, the government can announce major policy changes and can facilitate long-term plans, too. In summary, the distinction between an interim budget and a full-fledged budget lies in their scope, purpose, and the timeframe they cover.

How does the stock market react to the Interim Budget?

Now, let us move on to understand how stock markets react to these interim budgets.

Data analysis

I have analysed the last five interim budgets (i.e. 1998, 2004, 2009, 2014, and 2019) and how the stock market has reacted to them around the budget days.

To gauge its reaction, I have analysed the performance for three different periods:

- On the budget day

- Two days before the budget day. For example, in 2019, the budget was presented on 1st February. In this section, the stock market returns are calculated from 29th January to 31st January. The previous working day was considered if any day fell on a non-working day.

- Five days after the budget day. For example, for 2019, this will be measured from 1st February to 6th February. The next working day was considered if any day fell on a non-working day.

Following are the days considered for the analysis:

| Years | Budget Date | Previous Working Date | 2 Days Before | 5 Days After |

| 1998 | 25-March-98 | 24-March-98 | 20-March-98 | 30-March-98 |

| 2004 | 03-February-04 | 30-January-04 | 28-January-04 | 09-February-04 |

| 2009 | 16-February-09 | 13-February-09 | 11-February-09 | 24-February-09 |

| 2014 | 17-February-14 | 14-February-14 | 12-February-14 | 24-February-14 |

| 2019 | 01-February-19 | 31-January-19 | 29-January-19 | 06-February-19 |

| 2024 | 01-February-24 | 31-January-24 | 29-January-24 | 06-February-24 |

Analysing a single index will not do justice to the entire exercise. Therefore, I have analysed five indices viz. Nifty 50 Index, Nifty IT Index, Bank Nifty Index, Nifty FMCG Index and Nifty PSE Index.

Results

Indices History

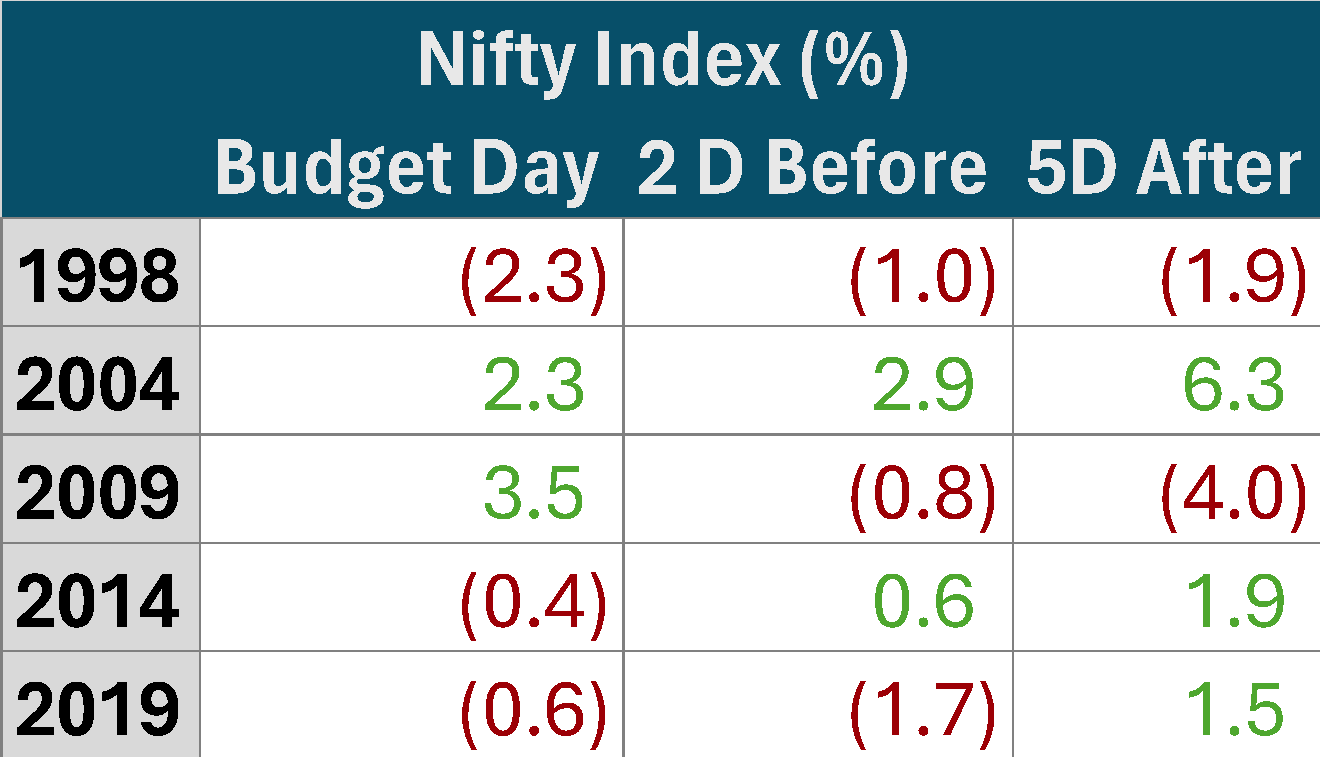

Nifty Index:

- Market mood dependency: Post-budget sentiment is closely linked to the market mood two days prior to the budget announcement. Over the last five interim budgets, the market’s performance after five days mirrored the trend set two days before the budget.

- Recent dampening: The last two interim budgets experienced a subdued impact on the market on the budget day, but they recovered after a week.

Other Indices:

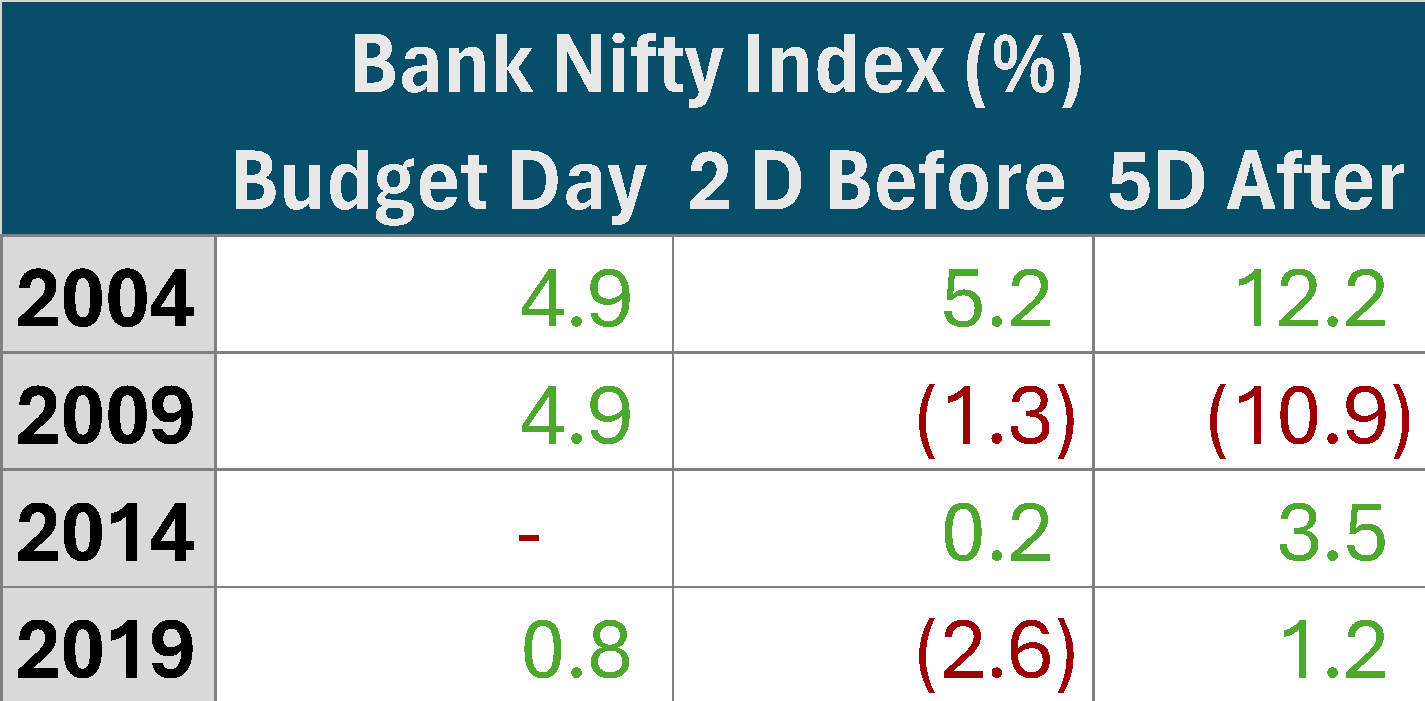

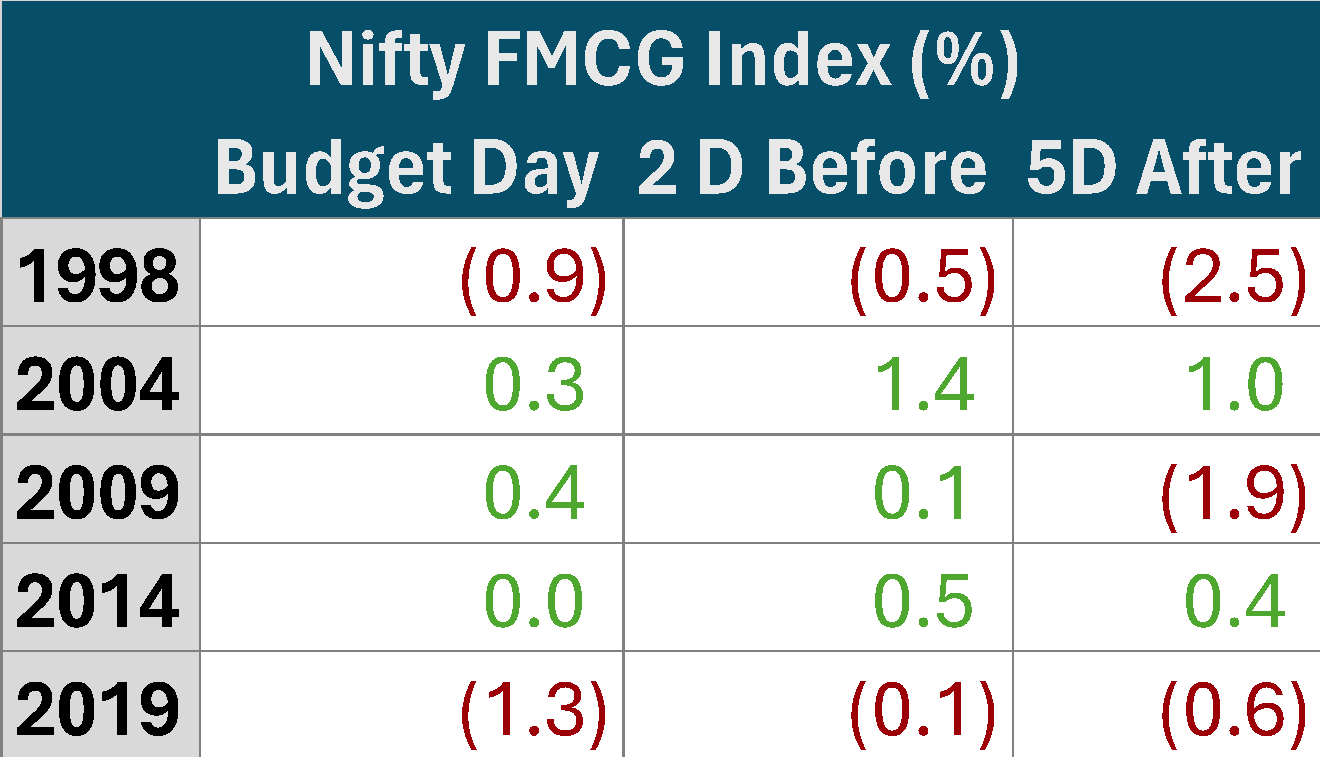

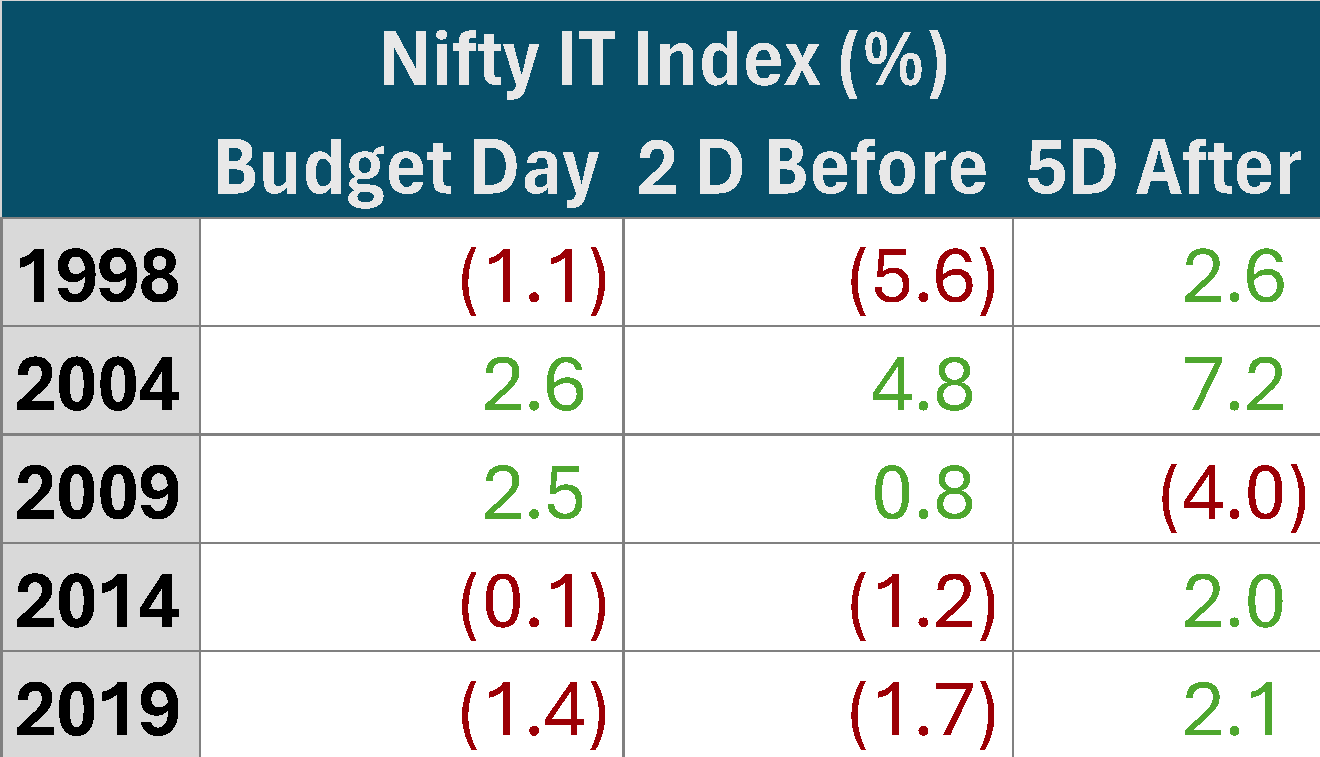

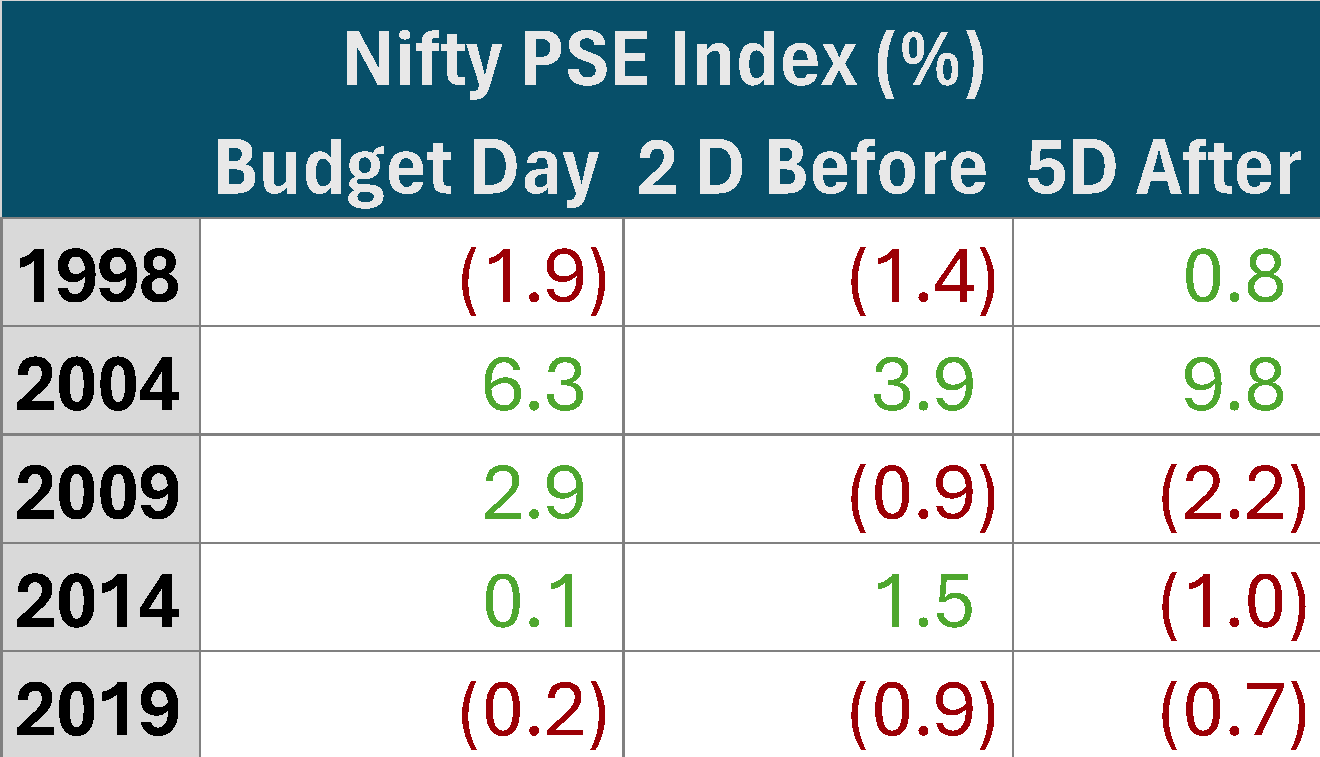

No clear pattern emerges out of the other indices. Banks have performed well overall in all the periods. FMCG nosedived the last time. The IT sector has not been impressed with the budget lately, showing a fall before and even on the budget day. PSEs had a negative growth the last time throughout this period.

Year-Wise Trends

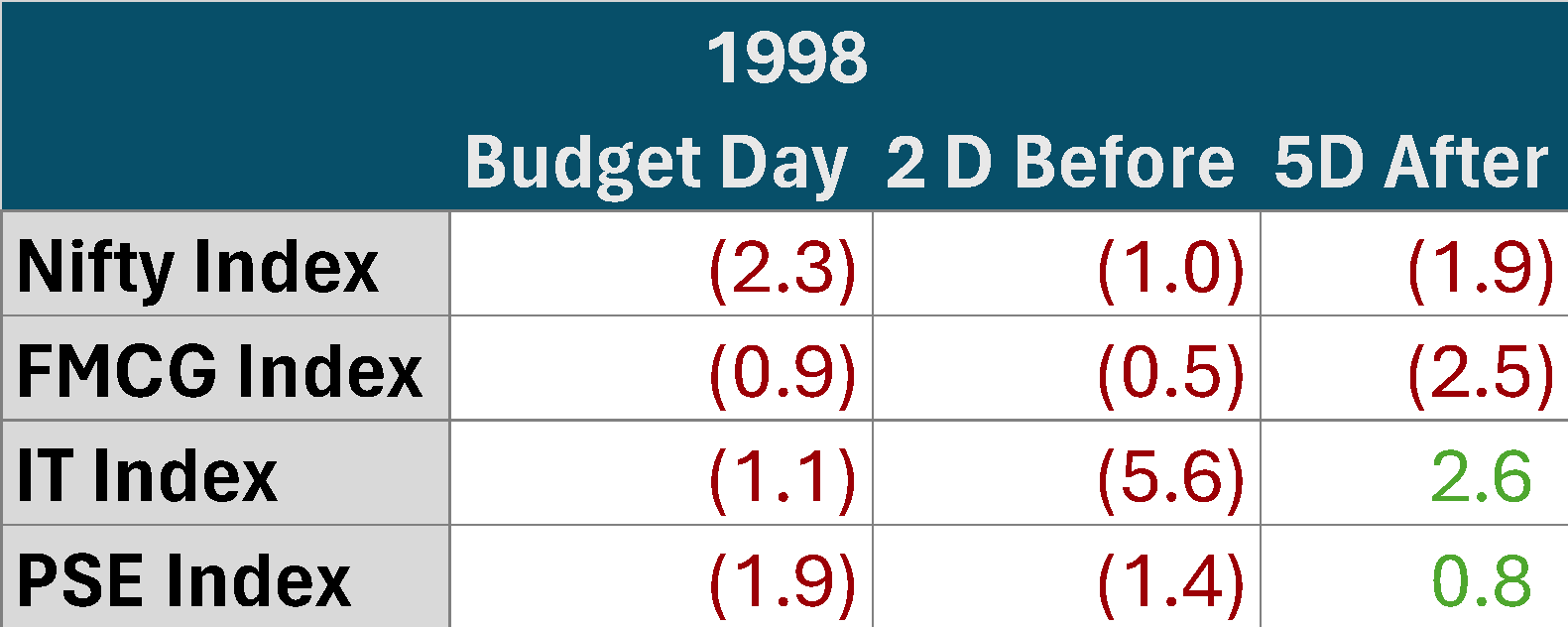

1998:

Minister: Yashwant Sinha (Speech link)

Background: Sanctions due to nuclear tests; East Asian Crisis

Real GDP Growth: FY 1998 = 4%; Prev. 5 yrs average = 6%

Highlights: Fiscal Deficit cuts, more funds to states, continuing momentum of 91 policy (Links – 1, 2, 3)

Markets:

- Market sentiment: Bearish.

- Notable performers: Nifty IT and PSE indices were the exceptions, showing positive growth after a week.

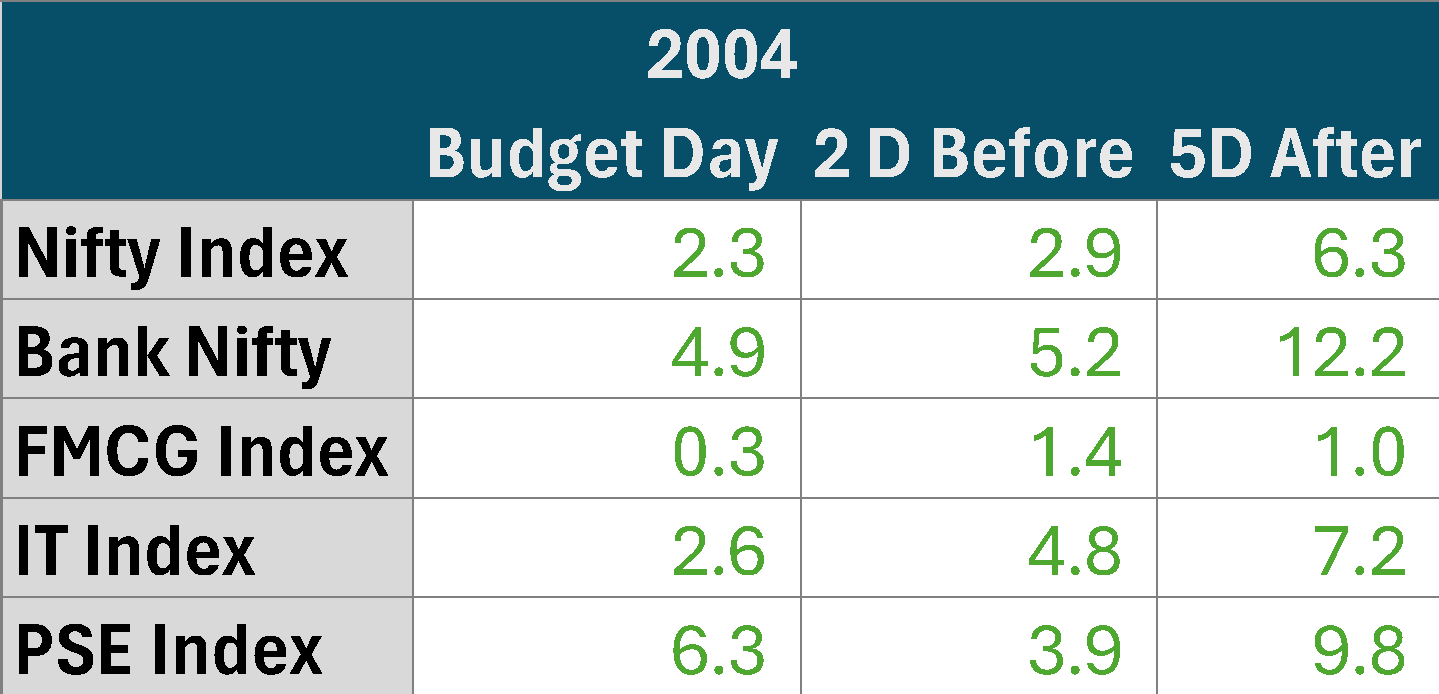

2004:

Minister: Jaswant Singh (Speech link)

Background: Mumbai blasts, Iraq war, India’s economic growth recognition around the world

Real GDP Growth: FY 2004 = 8%, Prev. 5 yrs average = 5%

Highlights: Extension of capital gains tax, direct tax benefits (Links – 1, 2, 3)

Markets:

- Market sentiment: Bullish, characterised by a positive trend.

- Overall performance: All indices recorded upward movement during the entire three performance review periods.

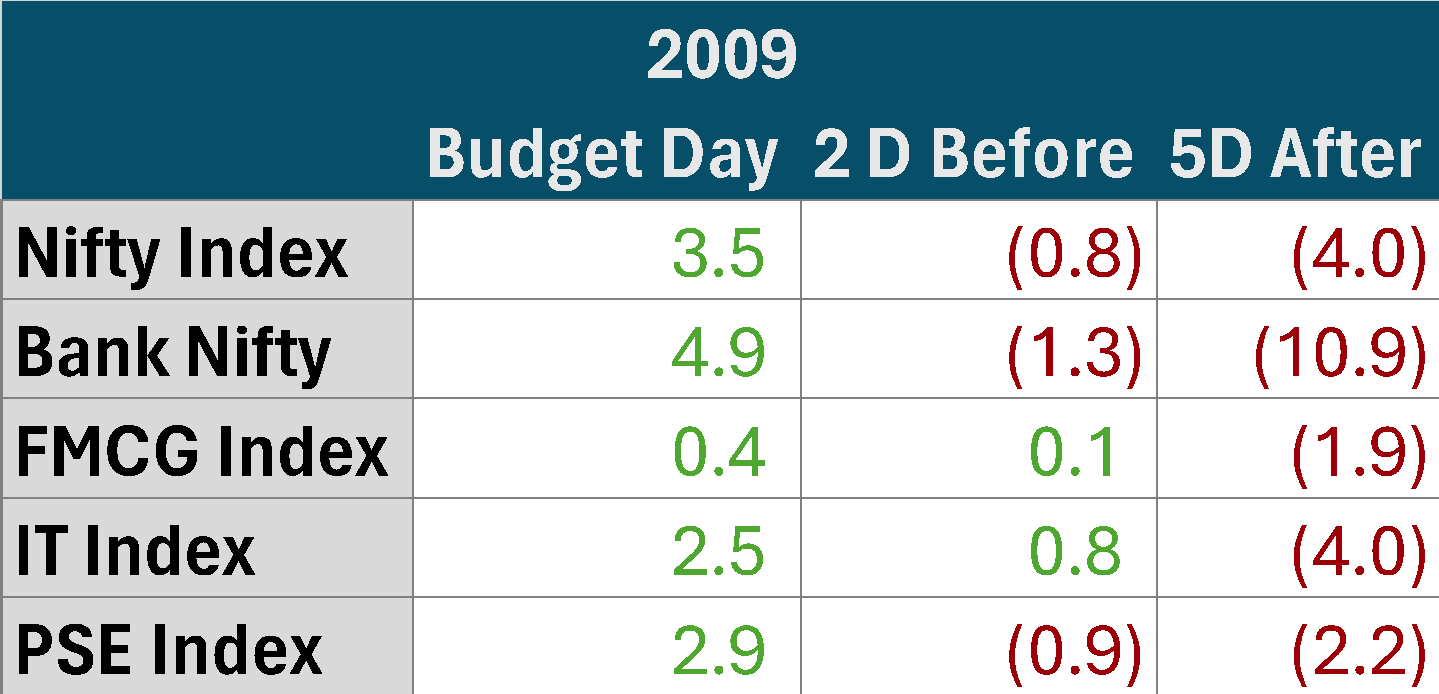

2009:

Minister: Pranab Mukherjee (Speech link)

Background: Global financial crisis, Commodity prices rise, Sustained economic growth

Real GDP growth: FY 2009 = 3%, Prev. 5 yrs average = 8%

Highlights: No economic stimulus, high subsidies, loan waivers (Links – 1, 2, 3)

Markets:

- Budget day impact: The market turned bullish.

- Pre-budget scenario: The market showed a flattish trend with predominantly red, except for the FMCG and IT sectors.

- Post-budget week: A shift with most sectors in the red.

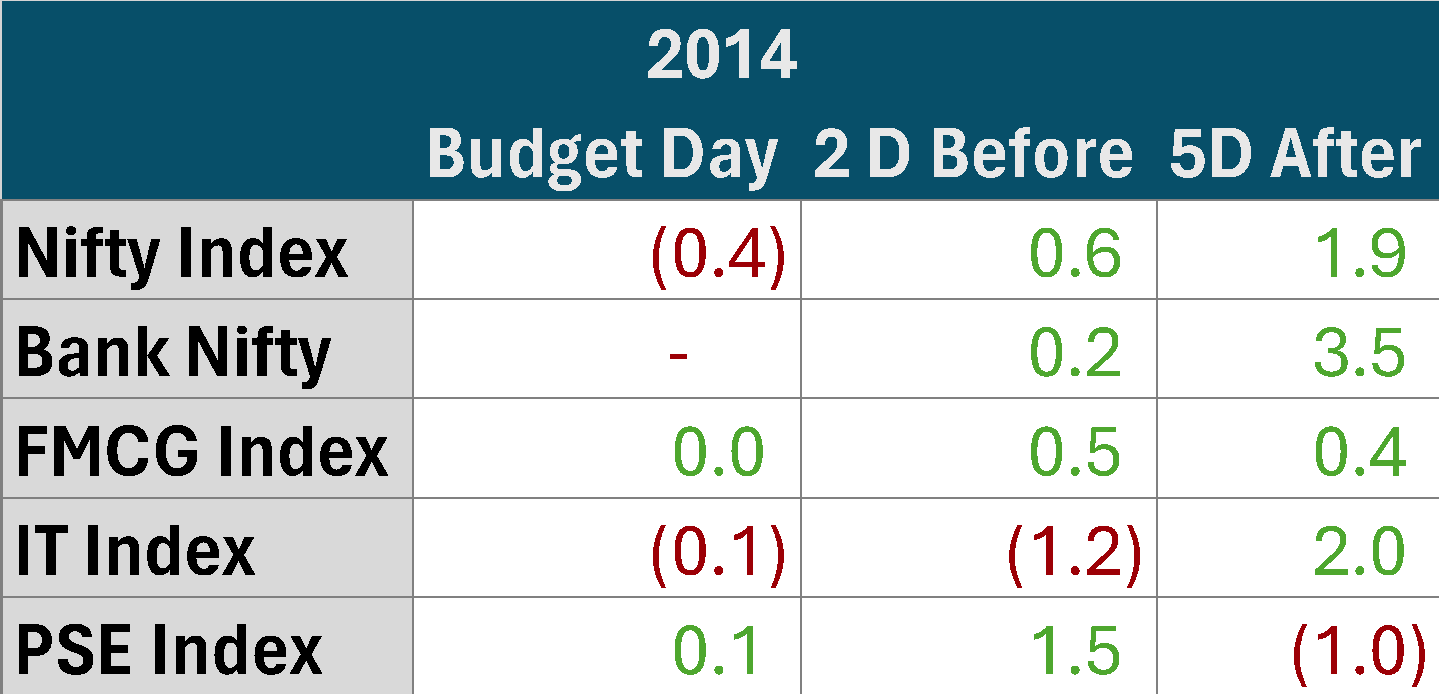

2014:

Minister: P Chidambaram (Speech link)

Background: Twin deficit, inflation

Real GDP growth: FY 2014 = 6%, Prev. 5 yrs average = 6%

Highlights: Excise duty cuts, fiscal consolidation. (Links – 1, 2)

Markets:

- Budget day impact: The market remained flat.

- Pre-budget scenario: Moderate excitement, with overall positive trends. The IT index was an exception, showing a decline.

- Post-budget: A general maintenance of positive momentum, with the PSE index in the red.

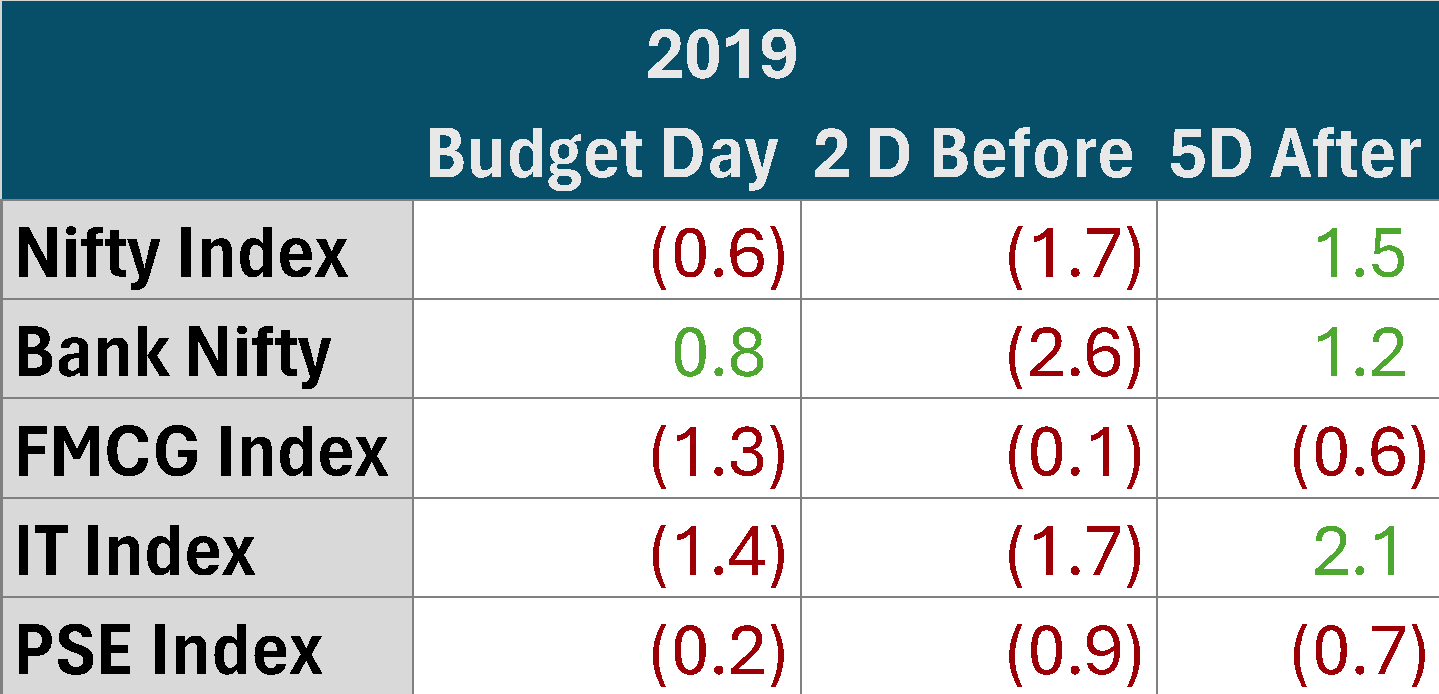

2019:

Minister: Piyush Goyal (Speech link)

Background: Lower commodity prices, lower inflation, macroeconomic stability

Real GDP growth: FY 2019 = 6%, Prev. 5 yrs average = 7%

Highlights: PM Kisan, Income tax rebate, informal sector pension (Links – 1, 2, 3)

Markets:

- Budget day and pre-budget market mood: Pessimistic, with the market in the red.

- Post-budget recovery: A positive shift was observed after a week.

To sum up

We all know the result seasons collide with the budget sessions. The financial position of a company, management’s announcements and valuations matter more in the overall scheme of things.

However, we cannot rule out the budget factor. Some budgetary announcements will impact stock markets. Sometimes, markets react to the overall sentiment or the mood that the budget sets in. However, markets adjust to the fundamentals, and the budget sentiment vanishes after a few days.

Therefore, this analysis should be read with caution. It does not in any way try to recommend any stock or sector. It is just an academic exercise.

But I would like to know how you think markets will react this year.

- Senior Citizens To Get Health Insurance? Facts Explained! - Apr 30, 2024

- How Stock Markets React to Interim Budgets: Cues From the History - Jan 31, 2024

- Top 5 Indian Economics Newsletters to Subscribe in 2024 - Dec 6, 2023