Ltd: A Proxy to Indian Manufacturing")

Last Updated on Jan 31, 2024 by Anjali Chourasiya

India is currently witnessing a significant transformation in its manufacturing sector. This shift is fueled by a range of government initiatives such as ‘Make in India’, ‘PM Gati Shakti National Master Plan’, and various Production-Linked Incentive (PLI) schemes. These efforts have boosted domestic manufacturing growth and attracted a considerable influx of Foreign Direct Investment (FDI). It has positioned India as a viable alternative to China’s manufacturing dominance.

China has been the biggest manufacturing hub, but now the tables have turned as China has experienced increased labour costs, directly reducing the advantage of low-cost manufacturing. Many countries, including the USA, have imposed trade restrictions on China due to international tension and conflicts. China has also faced significant environmental issues which have led to strict restrictions. Specific industries had gone into the over-capacity zone, leading to excess supply, which has hammered profitability. Last but not least, the appreciation of the Yuan has made exports expensive and reduced the competitiveness of Chinese products.

As a result, India’s young and vast workforce, coupled with substantial investments in infrastructure and favourable government policies, is setting a new stage for industries.

As manufacturing grows, the safety of people involved in manufacturing is also very important and here comes Mallcom (India) Ltd. The company is a one-stop solution for one of the widest ranges of full-body head-to-toe Personal Protective Equipment (PPE) products. They are also the largest exporters of PPE from India, exporting to 55+ countries across six continents.

Table of Contents

Global PPE market dynamics

The PPE industry, estimated at around $120 bn, is undergoing significant transformations. Historically, the PPE market has been heavily dominated by unorganised players, accounting for about 90% of the market. However, this landscape is rapidly changing due to stricter safety regulations and certification requirements. These new standards are increasingly challenging for unorganised players to meet, leading to a notable shift towards the organised sector. As a result, the market share of the unorganised sector has come down to 50%.

As more MNCs demand this critical use of protective equipment, the share of organised players will increase because MNC companies, like Honeywell, Reliance, and Indian Oil, won’t buy such critical equipment from a local manufacturer. This trend favours Mallcom as the company would benefit from two factors: market growth and the shift from an unorganised to an organised market.

Before we dive deep into Mallcom (India) Ltd, let’s have a brief look at the categories of PPE industries.

The industry is divided into three types of PPE categories.

- Category 1: It includes products that are good if you use them, but there is no harm or possibility of injuries or hazards if you don’t use them. Example: It is great if a sweeper wears a mask while sweeping the streets, but if he doesn’t, it’s still not a big issue.

- Category 2: These include products that are essential to use. If not used, they can cause injuries, but these injuries are less likely to be fatal. For example, the helmet factory workers wear can save them from minor injuries.

- Category 3: It includes products of very critical use, which, if not used properly, can lead to fatal injuries. An example is safety shoes worn while working in an electrical unit.

As the product becomes more critical, the market sees a corresponding decrease in fragmentation due to the increase in demand for certifications, thereby diminishing the presence of unorganised competitors. Additionally, the industry is experiencing a massive shift away from China to alternative markets, driven by supply chain complexities and the imposition of numerous trade restrictions.

On the other hand, India’s proactive approach in signing Free Trade Agreements (FTAs) with countries like the UAE and ongoing negotiations with others has opened new avenues for export-oriented companies. These FTAs facilitate easier and more cost-effective access to key markets, enhancing the export potential for Indian manufacturers. Additionally, the companies from the developed markets have started taking certifications and standardisation seriously, leading to an increased growth potential for the organised players in the market.

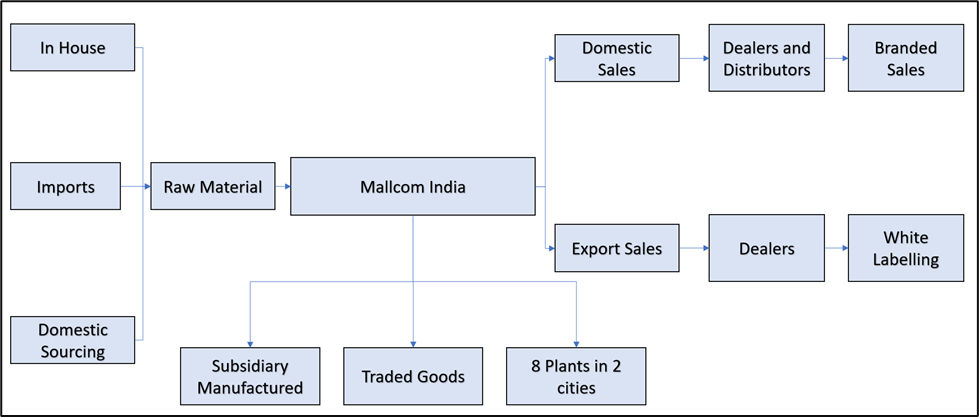

The business model of Mallcom (India) Ltd

Mallcom (India) Ltd has a strong presence on the domestic and global front. It sells through dealers and distributors under its brand name. The company also does white labelling through dealers in the global markets and for MNCs like Honeywell Caterpillar, Michelin, etc.

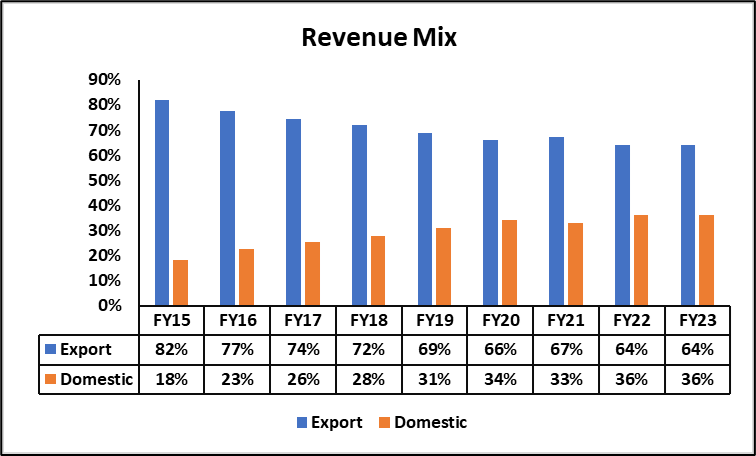

The key difference in both business models is the working capital cycle. On the domestic side, they have their brand and sell it through their dealers and distributors, so most of the sale happens through an on-the-spot payment mechanism, so the receivables are lower in the case of domestic sales. The management’s aim for a 50:50 mix between domestic and export sales is a strategic move towards gradual margin expansion, as selling under their brand gives them a comparatively higher margin.

The chart below shows that the share of domestic revenues has increased gradually. This also helps in reducing the working capital cycle.

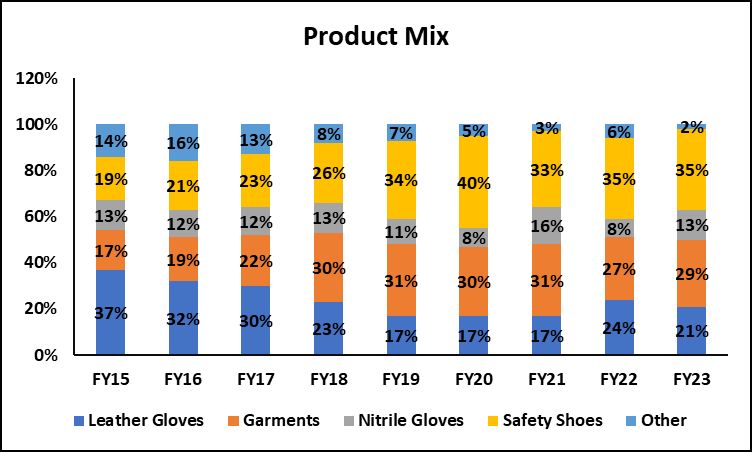

It is to be noted that safety shoes and garments are Category 2 and 3 products and hence have a comparatively higher margin. Gloves, on the other hand, are usually Category 1 and 2 products, so they have comparatively lower margins.

As we can see clearly from the chart above, the share of safety shoes has increased from 19% to 35% in FY 2023, and in H1 FY 2024, this share has gone to 42%. Garments, 17% of the entire business, went to 29% in FY 2023. Another point to note is that leather gloves are a highly fragmented market that doesn’t require any certification; hence, it is a lower gross margin business, and the management is reducing the leather gloves contribution in H1FY 2024. The contribution from leather gloves came down to 19%.

Management has constantly shifted from commodity Category 1 products to value-added Category 2 and 3 products; hence, one can see the evident gross margin expansion in the chart below.

Risks and challenges

Dependency on export incentives – As you can see in the table below, export incentives are a very significant part of the business. Relying heavily on export incentives can significantly impact the sustainability of margins and return ratios.

Frugal domestic market – Indians are very frugal when it comes to costs, and they want to produce each product at minimal costs. Going for branded products like those of Mallcom will increase the cost of production, and hence, many companies and labour specifically go for local or unbranded products.

Cost advantage to China in terms of raw materials – China might have slowed because of higher labour costs and environmental concerns. However, they still have an advantage in terms of raw materials, and hence, competing with China in Category 1 products is still a constraint.

Product quality issues in a fragmented market – During my personal visits to dealers and distributors, I observed a distinct trend: Mallcom’s shoes are primarily favoured by customers who are sensitive to pricing. On trying a pair myself, I noted that the shoes had notably thin soles, and the protective metal part placed near the toe, designed to safeguard against heavy objects falling on the foot, lacked sufficient cushioning. This resulted in pain in my toes. Such findings suggest that Mallcom’s strategy in the Indian market seems to be focused on capturing the lower-priced segment through branded sales, catering to budget-conscious consumers.

To sum up

The global manufacturing landscape is experiencing a pivotal shift, with India taking centre stage as a potent alternative to China. This change is exemplified by the ascent of companies like Mallcom (India) Ltd in the PPE industry. Mallcom, with its strategic focus on higher-margin Category 2 and 3 products and adaptation to the shift from unorganised to organised sectors, is well-positioned to leverage these evolving dynamics. However, challenges such as dependency on export incentives and a competitive market landscape remain. The future trajectory of Mallcom (India) Ltd, and indeed the broader Indian manufacturing sector, hinges on their ability to effectively navigate these opportunities and challenges, continuing to innovate and adapt in a rapidly changing global market.

Disclaimer: The views expressed by individuals are personal and do not represent the opinions or official stance of any firm, organisation, or entity. The information provided here is for informational purposes only and should not be considered as investment advice.

- Utility of Wealth in Gen Z and Their Spending Patterns - Apr 30, 2024

- Mallcom (India) Ltd: A Proxy to Indian Manufacturing - Jan 31, 2024

- Factors to Keep in Mind While Deciding Portfolio Weightage - Dec 21, 2023