Welcome to the April 2024 edition of Netra, where we present data-driven market insights that can inform your investing decisions.

This month, we’ll talk about the precious metals bull market that’s currently taking shape, the potentially unsustainable valuations of small- and mid-cap (SMID) companies, and the growing proportion of market capital that’s entering the stock market.

Table of Contents

Metals finally show their mettle

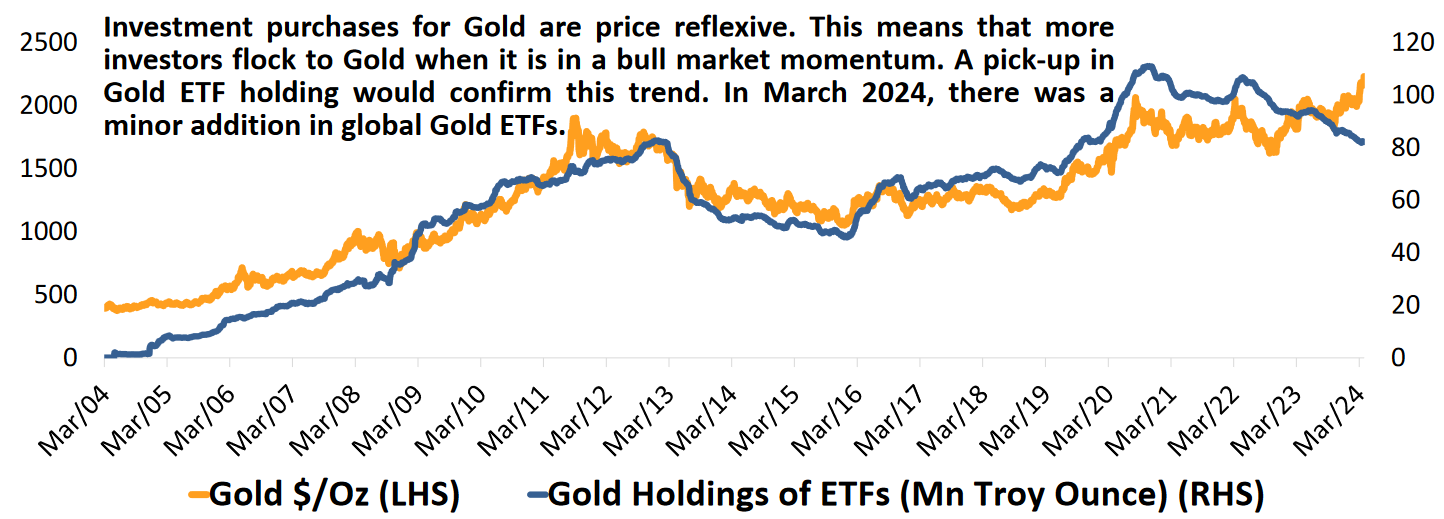

Gold prices, which have been sprinting upwards since the start of this year, finally hit new lifetime highs recently. There are several reasons for this, including central banks worldwide stocking up on the metal, ongoing geopolitical tensions, and anticipated interest rate cuts in the US.

Goldman Sachs recently stated that gold was in an “unshakeable bull market”, and set a price target of $2,700 per ounce by the end of this year. Nevertheless, March 2024 saw global gold ETF holdings fall by 14 tonnes; a rise in global gold ETF holdings would go a long way towards supporting the thesis that gold is in a bull market.

Source: Bloomberg, DSP; Data as of Mar 2024

What about silver? Well, given that silver has now pushed through a key resistance at the $26 mark, it certainly seems like a broader precious metals bull market is coming together.

Ever since Nixon delinked the dollar from gold in 1971, gold has outperformed silver by a huge margin. However, when a precious metals bull market is in place, silver tends to have a very high relative outperformance score relative to gold. Thus, it might be a good idea to add both metals to your portfolio right now.

SMID valuations touch the sky

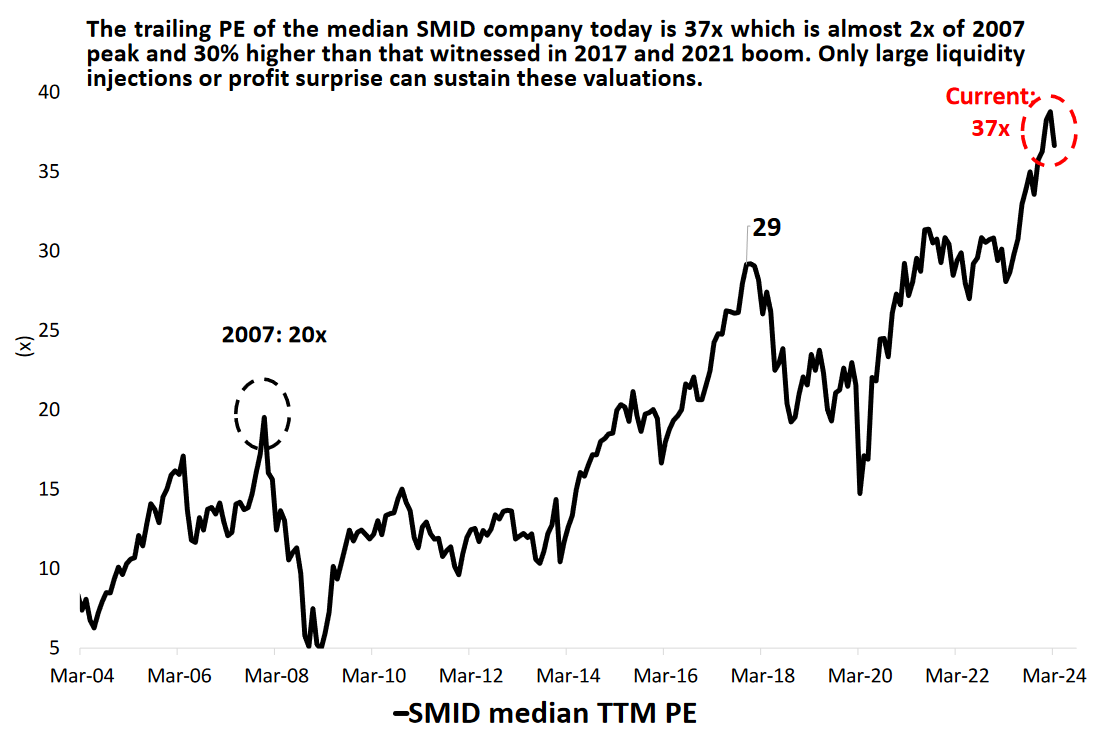

In March 2024, the median valuation (on a trailing price-to-earnings basis) for the SMID (small- and mid-cap) universe peaked at nearly double (37x) of what it was at the 2007 bull market peak (20x).

Source: Nuvama Research, DSP; Data as of Mar 2024

How should you react to this? While SMID valuations might seem excessive right now, history indicates that such apparent excesses can continue in the same direction indefinitely. However, this doesn’t mean that it pays to invest in potentially overvalued stocks, nor that you should take unnecessary risks.

Current SMID valuations offer little comfort: they are likely to be unsustainable without large liquidity injections or surprise profits. Thus, for the most part, you’ll need to rely on fundamentals to find opportunities in this space.

Forward returns could be more subdued

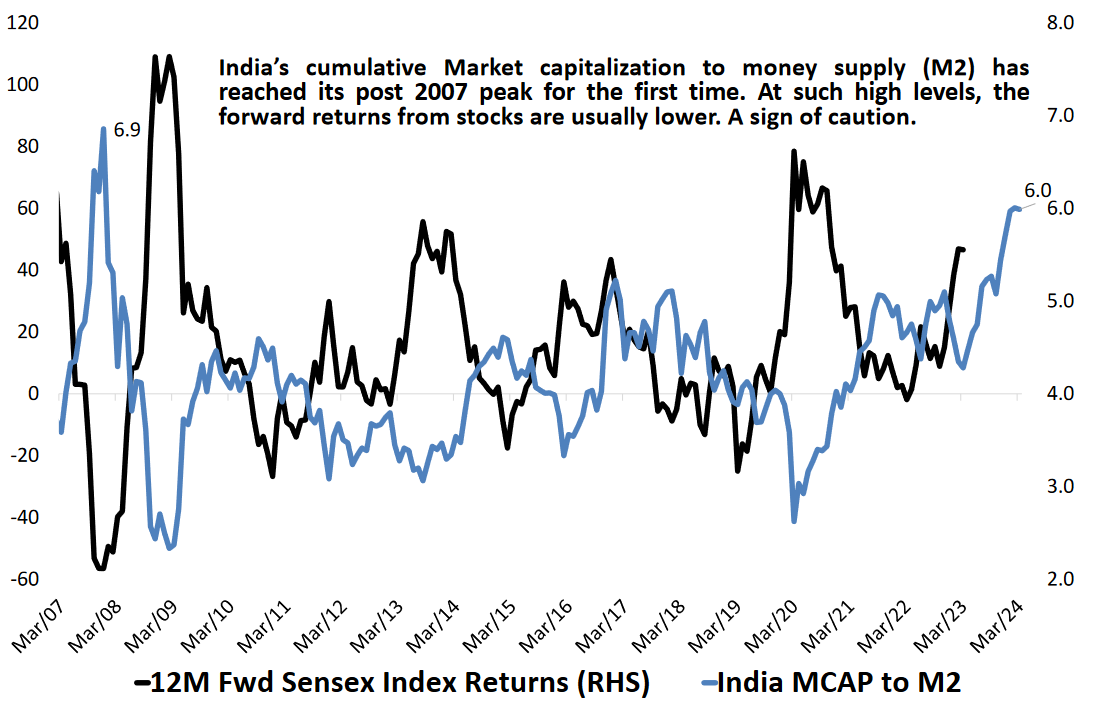

Currently, the ratio of India’s equity market capitalisation to its money supply (M2) is at its highest level since the 2003-07 stock market peak. M2 is a broad measure of the money supply that includes cash, checking deposits, savings deposits, and certain types of time deposits and money market funds.

As can be seen from the graph below, the market-cap-to-M2 ratio is, for the most part, negatively correlated with the forward returns from stocks. In other words, when this ratio is at a relatively high level, the forward returns from stocks are usually relatively low. Thus, it might be prudent to factor this metric into your near-term investing decisions.

Source: Bloomberg, DSP; Data as of Mar 2024

The bottom line

Given the rosy prospects for gold and silver for the rest of this year, it might be worth adding them to your portfolio if you haven’t already done so. In addition, the high valuations in the SMID space should be responded to with a fundamentals-first approach. Lastly, the currently high market-cap-to-M2 ratio should be looked upon as a cautionary sign.

For more actionable insights backed by data and analyses, we invite you to read the latest edition of Netra in its entirety.

The bottom line

Despite global uncertainties such as ongoing wars, geopolitical crises, and surging oil prices, India has stood its ground. The economy is on the path to normalcy, corporates have strengthened their balance sheets, there is increased capital expenditure in infrastructure, and the banking sector is in great shape. It can be a great time for India to push its growth horizon.

Disclaimer

In this material DSP Asset Managers Pvt. Ltd. (the AMC) has used information that is publicly available, including information developed in-house. Information gathered and used in this material is believed to be from reliable sources. The AMC however does not warrant the accuracy, reasonableness and / or completeness of any information. The above data/ statistics are given only for illustration purpose. The recipient(s) before acting on any information herein should make his/ their own investigation and seek appropriate professional advice. This is a generic update; it shall not constitute any offer to sell or solicitation of an offer to buy units of any of the Schemes of the DSP Mutual Fund. The data/ statistics are given to explain general market trends in the securities market and should not be construed as any research report/ recommendation. We have included statements/ opinions/ recommendations in this document which contain words or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risks or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and/ or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

- Netra April 2024 Market Analysis Report – 3 Key Takeaways! - Apr 26, 2024

- Netra March 2024 Market Analysis Report – 3 Key Takeaways! - Mar 20, 2024

- Trading Actively? You Need “Something Just Like This” - Mar 15, 2024